Independent Sponsor LOI Playbook (65-75% Close, 90-Day Runway) in 2026

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Quick answer: The independent sponsor LOI closes at 65-75% (versus 80-90% for funded PE) when six terms are negotiated correctly: 90-day exclusivity with a 30-day auto-extension, 5-10% deposit in escrow, a capital-raising contingency paired with a soft support letter, 4-6x EBITDA price with 10-40% seller rollover, data room access within 5 days post-LOI, and an explicit broken-deal cost-share clause with your capital partner. Get any of the first three wrong and the deal dies in week 4 — not because the seller pulls out, but because your capital partner cannot complete diligence inside your exclusivity window. This playbook walks through each clause first-time independent sponsors most often regret signing, with the 2025 Citrin Cooperman and Axial benchmarks that anchor each term to current market practice.

This playbook is written for three specific readers, and each one negotiates the LOI from a different chair: the seller-side M&A advisor or transaction counsel reviewing an inbound LOI from an independent sponsor and deciding whether to recommend a counter, an extension, or a pivot back to a funded PE bidder; the first-time independent sponsor drafting an LOI as the opening bid on a $10-50M lower-middle-market target without a committed equity check yet; and the M&A advisor or sell-side banker coaching a first-time founder-seller through an LOI negotiation where the buyer is fundless and the family-office capital stack is still being assembled. Each chair reads a different clause first — the seller's counsel jumps to exclusivity and deposit; the sponsor jumps to financing contingency and rollover; the sell-side coach jumps to broken-deal cost allocation. The risk-severity matrix below is built to be readable from any of those three entry points.

The single hardest question in this entire process is not "what should my LOI say?" — it is "which clauses will sellers regret signing six weeks from now, when capital partners are still in diligence and the exclusivity clock has burned to 30 days?" The answer is the eight clauses below — exclusivity duration, deposit size, financing contingency language, capital partner support letter timing, rollover percentage, earnout structure, retrade triggers, and broken-deal cost allocation — every one of which has a default form that favors funded PE and a sponsor-friendly form you have to ask for. I spent two years at Backed VC and Target Global watching deals die at the 4-week mark, and the pattern is almost always the same: the sponsors who close have their capital partner data room ready in the 72 hours after signing. The ones who lose exclusivity spend the first two weeks assembling documents while their 90-day clock burns.

Quick LOI Term Reference

Use this 1-page summary to triage which terms to negotiate hardest before turning to the deeper playbook below. The risk levels reflect Peony's framework: a Deal-Killer term, if missed, ends the deal entirely; a Margin-Eroder term shifts dollars to the seller or capital partner without breaking the deal; a Cosmetic term affects deal mechanics or perception but rarely determines outcome.

| LOI Term | IS Target | PE Norm | Risk Level | Deal-Killer if... |

|---|---|---|---|---|

| 1. Exclusivity | 90 days + 30-day auto-extension on milestones | 45-60 days | Deal-Killer | You sign at 60 days and capital partners need 70+ to close |

| 2. Deposit | 5-10% of purchase price in escrow | Often waived for funded PE | Deal-Killer | You offer below 3% on a deal where seller has competing funded PE bid |

| 3. Financing contingency | Capital-raising contingency + soft support letter | No financing contingency | Deal-Killer | You sign with no support letter and your sole capital partner walks in week 4 |

| 4. Purchase price and structure | 4-6x EBITDA, 60-80% cash, 10-40% rollover, optional earnout | 8-12x EBITDA, 80-100% cash | Margin-Eroder | You over-pay on multiple to win bid and capital partners reject thesis |

| 5. Diligence access and milestones | Data room within 5 days, mgmt meetings within 15, QoE within 10 | Standard milestones embedded | Margin-Eroder | Seller delays data room access by 3+ weeks and your 90-day clock effectively becomes 70 |

| 6. Broken-deal cost allocation | Cost-share clause with capital partner | N/A — fund absorbs | Cosmetic | Deal dies and you absorb $150K+ in legal/QoE/accounting fees alone |

The "Deal-Killer if..." column is what to game-plan against in negotiation: not the average outcome, but the failure mode that ends the deal.

Why IS LOIs are structurally different from PE fund LOIs

A traditional PE fund writes an LOI backed by committed capital. An independent sponsor writes an LOI backed by relationships and a thesis. This distinction changes everything about how the LOI should be structured.

| Dimension | Independent sponsor | Funded PE |

|---|---|---|

| Capital at LOI signing | None committed — soft-circled or raised post-LOI | Blind-pool fund, capital available immediately |

| Support letters | 55.4% provide pre-LOI, down from 68.2% in 2023 | Not needed — fund exists |

| Minimum exclusivity needed | 90 days with auto-extension | 45-60 days typical |

| Seller perception | 73% of M&A advisors say IS take longer to close | Funded buyer = perceived certainty |

| Timeline to close | 60-120 days | 45-75 days |

| LOI-to-close conversion | 65-75% of exclusive LOIs | Estimated 80-90% |

| Diligence cost risk | Sponsor bears costs personally until capital commits | Fund absorbs from management fees |

Sources: Axial 2025 Independent Sponsor Report; McGuireWoods 2024 Deal Survey; Citrin Cooperman 2025.

The 73% figure is the number that should shape every LOI term you negotiate. Nearly three-quarters of M&A advisors believe you are a slower close than a funded buyer. Your LOI needs to preemptively address this perception.

The 6 LOI terms that determine whether your deal closes

1. Exclusivity: 90 days minimum, auto-extension mandatory

This is the single most important term. Your capital partners need 3 to 4 weeks for their own diligence. You need 4 to 6 weeks for yours. Definitive agreement negotiation takes another 2 to 4 weeks. A 45-day exclusivity window that works for funded PE leaves you with roughly zero margin.

Negotiate 90 days with a 30-day automatic extension triggered by demonstrable deal progress (completed QoE, capital partner term sheet, draft purchase agreement). If a seller offers only 60 days, you are entering the deal with a structural disadvantage that no amount of hustle can fix.

2. Deposit: 5-10% of purchase price in escrow

Standard in lower-middle-market acquisitions. For a $25M deal, this means $1.25M to $2.5M at risk. Nearly 90% of private-target M&A deals include escrow according to the SRS Acquiom 2025 Deal Terms Study, and the median separate purchase price adjustment escrow has held at roughly 1% of transaction value across recent years.

Your deposit is one of the few concrete signals of certainty you can offer a seller before capital is committed. Structure it with clear refund conditions tied to specific diligence findings — this protects your downside while still demonstrating financial commitment. If you cannot fund the deposit personally, discuss with your lead capital partner whether they will backstop it as part of their pre-LOI engagement. Share deposit terms securely with password-protected document access to prevent sensitive pricing from reaching competing bidders.

3. Financing contingency: include it, but pair it with a support letter

Include a capital-raising contingency clause — you are raising equity after the LOI, and pretending otherwise is a liability. But pair the contingency with at least one capital partner support letter. According to Axial's 2025 report, 55.4% of independent sponsors now provide support letters pre-LOI. Even a soft letter naming a family office or SBIC fund that has reviewed the thesis signals that your capital is more than theoretical.

The trend is shifting toward post-LOI letters — 39.2% of sponsors now provide them post-LOI, up from 18.2% in 2023. But in competitive situations, a pre-LOI letter still differentiates you from the other fundless buyer who has nothing but a handshake. The deeper dive on how pre-LOI versus post-LOI letters work — including sample language and capital partner hedge clauses — is in the pre-LOI vs post-LOI section below.

4. Purchase price and structure: the IS advantage

Independent sponsor deals closed at 4x to 6x EBITDA in 54% of transactions in 2024, with 37% at 6x to 8x according to Citrin Cooperman 2025. Compare this to PE fund medians of 10.2x to 14.9x. Your purchase price should reflect LMM fundamentals, not PE auction dynamics. Citrin Cooperman's 2025 commentary notes that quality assets that used to trade at 4x to 6x are now changing hands at 6x to 9x — the spread between mediocre and quality LMM assets has widened.

Structure the consideration to leverage your flexibility advantage: 60 to 80% cash at close, with the remainder in seller rollover equity, earnouts, or seller financing. Short-term earnouts appeared in 32.5% of IS deals in 2024, down from 43.8% in 2023, while management incentive pools rose to 18.2% from 6.3%. The trend is away from deferred compensation and toward aligned incentives. For the deeper economics negotiation playbook — promote, GP commit, fee structure — see the capital raising playbook.

5. Diligence access and timeline milestones

Build specific milestones into the LOI: data room access within 5 business days, management meetings within 15 days, QoE report commissioned within 10 days. These milestones protect both parties — the seller sees progress, and you have contractual cover if access is delayed.

QoE EBITDA discrepancies were the number 2 reason LOIs broke in 2025 at 21.3% according to the Axial Dead Deal Report, more than doubling from 10.6% in 2023. If your deal budget allows it, commission the QoE before signing the LOI. A $30,000 to $75,000 pre-LOI QoE dramatically accelerates capital partner diligence because partners can evaluate adjusted EBITDA from day one.

6. Broken-deal cost allocation

Emerging sponsors often overlook this. If the deal falls apart after you have spent $150,000 on legal, accounting, and diligence fees, who absorbs that cost? According to practitioners at OpusConnect, broken deal costs can reach hundreds of thousands of dollars.

Negotiate a cost-sharing arrangement with your capital partner upfront. If they walk after completing their diligence, they should share a defined portion of sunk costs. Without this protection, a failed deal can wipe out a first-time sponsor financially.

The LOI Risk-Severity Matrix — Peony's framework for prioritizing negotiation

Most first-time sponsors negotiate every LOI term equally. Experienced sponsors negotiate the deal-killers hard, accept the margin-eroders with caveats, and concede the cosmetic terms to build seller goodwill. The matrix below is how Peony categorizes the six LOI terms across three axes: severity (what happens if you lose this point), negotiability (how movable the seller is), and cost of getting it wrong (dollar impact and timeline impact).

| LOI Term | Severity | Negotiability | $ Impact if Wrong | Timeline Impact if Wrong |

|---|---|---|---|---|

| 1. Exclusivity | Deal-Killer | Medium | Total deal value lost ($1M-$15M+ equity check) | Restart at month 3-4 |

| 2. Deposit | Deal-Killer | Hard | $500K-$2M+ at risk if you over-commit | Immediate (escrow funded) |

| 3. Financing contingency | Deal-Killer | Soft | Total deal value lost if no contingency | Immediate (signing terms) |

| 4. Purchase price and structure | Margin-Eroder | Hard | $500K-$5M on multiple, $200K-$1M on structure | Marginal |

| 5. Diligence access and milestones | Margin-Eroder | Soft | $50K-$200K (pace of QoE, lost weeks) | 1-3 weeks of compressed runway |

| 6. Broken-deal cost allocation | Cosmetic | Soft | $50K-$300K if deal dies | Post-deal financial recovery |

How to use this matrix in negotiation. Spend your hardest negotiating capital on terms 1 and 3 — both are Deal-Killers and term 3 (financing contingency) is Soft on negotiability, meaning sellers usually accept reasonable contingency language if you frame it well. Term 2 (deposit) is also a Deal-Killer but Hard on negotiability — sellers rarely accept below 3 to 5%, so calibrate to market rather than fight it. Term 4 (purchase price) is where most sponsors waste energy; it is Hard to move and the dollars are smaller than people think relative to a 3-year value creation plan. Term 5 (diligence access) is Soft — push for explicit milestones because most sellers' M&A advisors agree, and the milestones protect you from the seller's slowness. Term 6 (broken-deal cost) is the term to concede most graciously to seller goodwill while protecting yourself with a parallel agreement at the capital partner level instead.

The matrix also explains a counterintuitive pattern Peony has observed: first-time sponsors who walk away from deals with bad exclusivity terms (60 days, no auto-extension) close their NEXT deal at 90 days far more often than sponsors who sign anyway and learn the hard way. Walking from a Deal-Killer term builds reputation; signing into one burns equity and reputation simultaneously.

Real-deal LOI dissections from public IS transactions

The LOI playbook is informed by what actually happened in publicly disclosed lower-middle-market transactions. Below are three deal archetypes with the LOI term that determined outcome — drawn from SEC filings, public press releases, and conference disclosures rather than confidential client data.

Archetype 1: The 90-day exclusivity with explicit 30-day extension (McEwen / Canadian Gold Corp, July 2025)

Deal: McEwen Inc. signed a binding letter of intent in July 2025 to acquire all outstanding shares of Canadian Gold Corp in a stock-for-stock transaction. EV: Stock-for-stock; precise enterprise value not disclosed in the initial 8-K. Sector: Mining / natural resources. Year: 2025.

Critical LOI term: Exclusivity of 90 days from execution, with a written-agreement 30-day extension clause if parties were continuing to negotiate definitive agreements in good faith. Lesson: Even in public-company stock deals, the 90-day-plus-30 framework is the practitioner standard — and the explicit extension clause (rather than implicit goodwill) is what distinguishes well-drafted LOIs from improvised ones. For independent sponsors writing LOIs on private LMM deals, this clause structure is the floor, not the ceiling. (Source: McEwen Inc. SEC 8-K filing, July 2025.)

Archetype 2: The retrade-triggered exclusivity termination (general LMM pattern)

Deal archetype: Lower-middle-market services acquisition where buyer attempts retrade after QoE finds adjusted EBITDA discrepancy. EV: Typical $15M to $35M. Sector: Services (industry-agnostic). Year: Pattern observed across 2023-2025 LMM transactions.

Critical LOI term: Many LMM LOI templates now include language stating that if buyer attempts retrade or proposes a significant change in price or terms, the seller's exclusivity obligation terminates and the seller may resume marketing the asset. Lesson: Sellers' M&A advisors are now systematically inserting this clause to protect against post-LOI retrade — which has become more common as QoE-driven EBITDA discrepancies (21.3% of broken IS deals in 2025 per Axial Dead Deal Report) push buyers to reduce price mid-exclusivity. As the IS buyer, you should accept this language because attempting retrade typically signals a deal that should be re-priced or walked anyway. The deeper insight: if you commission your QoE pre-LOI ($30K to $75K cost), you avoid the retrade scenario entirely because EBITDA discrepancies surface before signing. (Source: M&A LOI exclusivity drafting guidance, multiple LMM advisor publications 2024-2025.)

These archetypes reinforce a single point: the LOI terms that determine outcome are not novel. They are well-documented in public filings and practitioner research. The independent sponsor advantage is treating these terms as a system, not as standalone clauses.

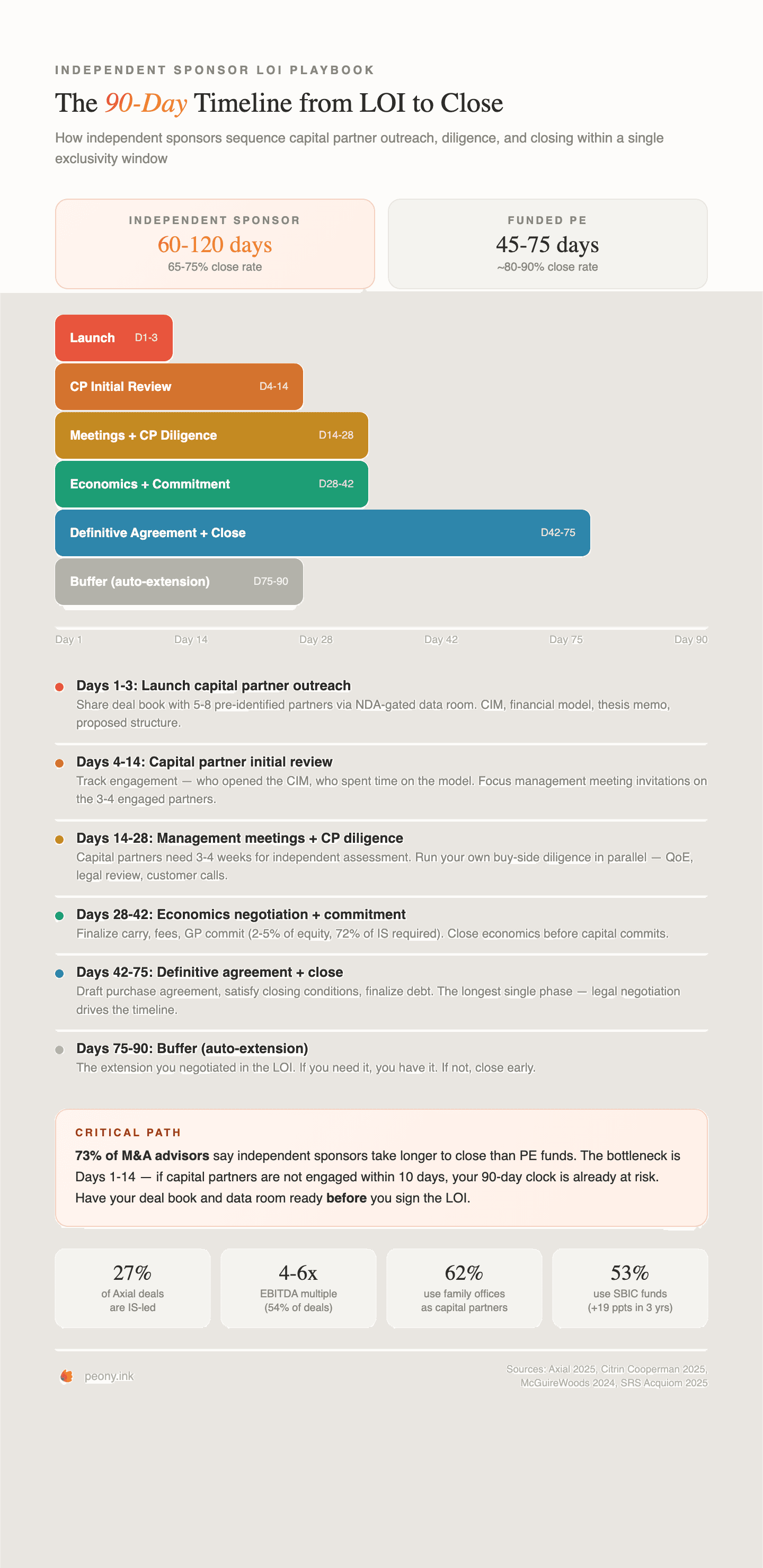

The 90-day timeline: what actually happens week by week

Days 1-3: Launch capital partner outreach. Share your deal book with 5 to 8 pre-identified capital partners through NDA-gated data room access. Your deal book should include the CIM, your financial model, investment thesis memo, preliminary diligence findings, proposed capital structure, and proposed economics. If this package is not ready on day one, you are already behind. For the full 10-section deal book breakdown see the deal book guide.

Days 4-14: Capital partner initial review. Page-level analytics show which partners actually opened your materials and how long they spent on the financial model versus the CIM cover page. Focus management meeting invitations on the 3 to 4 partners showing genuine engagement.

Days 14-28: Management meetings and capital partner diligence. Your capital partners need 3 to 4 weeks for their independent assessment. During this period you are also running your own buy-side diligence — reviewing the seller's data room, commissioning the QoE if not already done, and validating the thesis.

Days 28-42: Economics negotiation and commitment. Negotiate final terms with your 1 to 2 serious capital partners. GP commit is now standard — 72% of IS are required to contribute 2 to 5% of the equity check according to Citrin Cooperman 2025. Close the economics before your partners commit capital. Use e-signatures to execute term sheets and subscription documents directly in the data room. (For pre-LOI cultivation and term sheet economics negotiation, see the capital raising playbook.)

Days 42-75: Definitive agreement and closing conditions. Draft and negotiate the purchase agreement, satisfy closing conditions, finalize debt financing, and prepare for close.

Days 75-90: Buffer. The automatic extension you negotiated in the LOI. If you need it, you have it. If you do not, you close early and the seller is happy.

The dual data room: the operational pain point that kills deals

Independent sponsors manage two data rooms simultaneously — one from the seller (receiving diligence materials) and one for capital partners (sharing the investment opportunity). This dual workflow is unique to the IS model and is the single biggest source of operational friction.

Your capital partner data room structure

Stage 1 (Day 1 — all partners):

- Investment thesis memo

- Confidential Information Memorandum

- Sponsor track record and credentials deck

- High-level financial summary and key metrics

- Proposed capital structure (sources and uses)

- Preliminary value creation plan

Stage 2 (Day 7-10 — engaged partners only):

- Quality of earnings report (or preliminary financial analysis)

- Detailed financial model with sensitivity tables

- Customer concentration analysis

- Legal and regulatory summary

- Management presentation notes

Stage 3 (Day 21-28 — committed partners only):

- Governance term sheet (board composition, consent rights)

- Promote and carry schedule with hurdle tiers

- Subscription documents

- Capital partner reporting framework

- Broken-deal cost allocation agreement

Use per-viewer staged access to expand each partner's permissions as they progress — no need to create separate data rooms. Peony Business ($40/admin/month) includes everything IS workflows require: NDA gates, dynamic watermarks, screenshot protection, AI-powered Q&A, and full data room capabilities. Page-level analytics reveal who moved past the CIM to the financial model versus who downloaded Stage 1 materials and went silent. The full 42-document checklist by stage is in the data room checklist.

Pre-LOI vs post-LOI capital partner support letters: when each works

The single most contentious LOI question Peony hears from first-time sponsors is whether to provide a capital partner support letter pre-LOI or post-LOI. The market is mid-shift: 55.4% pre-LOI (down from 68.2% in 2023) and 39.2% post-LOI (up from 18.2%) per Axial 2025. A small but growing segment of sponsors close deals with no support letter at all — typically experienced sponsors with proprietary deal sourcing. The right answer depends on three deal characteristics — competitive intensity, sponsor experience level, and deal size — not a one-size-fits-all rule.

When pre-LOI support letters win

Pre-LOI letters are mandatory in three scenarios.

Competitive bid situations. When the seller's M&A advisor is running a structured process with 2 or more bidders, your pre-LOI letter is the only way to neutralize the funded-PE certainty advantage. The letter does not need to commit capital — it needs to name a specific capital partner who has reviewed the thesis and confirms interest in pursuing diligence. Even a soft letter saying "we have reviewed the thesis and confirm our interest in evaluating co-investment alongside the sponsor" beats no letter in a competitive process.

First-time sponsors. If you have no prior closed IS deal, the seller has zero evidence you can deliver. The pre-LOI letter is the substitute. A first-time sponsor with a soft pre-LOI letter from a recognized SBIC or family office passes the seller's "is this real" test; a first-time sponsor with no letter usually does not. Repeat sponsors with a track record can afford post-LOI because their reputation carries the certainty signal.

Large deals ($35M+ EV). At larger deal sizes the equity check is bigger, the number of capital partners is larger, and the seller's risk if you fail to close is more concentrated. Pre-LOI letters at this size signal that the lead capital partner exists and is engaged — without which the seller is taking a meaningful concentration risk by removing the asset from market for 90 days.

When post-LOI is acceptable

Post-LOI letter assembly works in three scenarios.

Warm repeat capital partner relationships. If your lead capital partner is a repeat investor who has executed 2 or more prior deals with you, a phone call commitment is often equivalent to a letter. The seller's M&A advisor will accept post-LOI letters when the sponsor can credibly name the partner and the partner can confirm engagement on a brief diligence call.

Smaller deals ($10M to $20M EV). At smaller deal sizes the equity check is $3M to $8M, which a single family office or HNWI can backstop without a syndicate. The post-LOI letter is sufficient because the capital concentration is less material to the seller.

Sole capital partner structures. If your deal is funded entirely by one family office or one SBIC, the post-LOI letter from that single partner can land in week 1 of exclusivity and is structurally adequate. The pre-LOI letter is more valuable when you are syndicating equity across 3 or more partners and need to demonstrate aggregated commitment.

What language to use in the letter

Capital partner support letters are short — typically 1 to 2 pages — and follow a recognizable structure. Useful directional language (NOT a template; consult counsel for actual drafting) includes:

-

Engagement framing: "[Capital Partner] has reviewed the investment thesis for [Target Company] presented by [Sponsor] and confirms its interest in pursuing further diligence with the goal of co-investing alongside the sponsor in the proposed transaction."

-

Diligence scope: "Subject to satisfactory completion of confirmatory diligence — including but not limited to financial, operational, legal, and regulatory review — [Capital Partner] anticipates evaluating an equity commitment in the range of [$X to $Y]."

-

Timeline framing: "[Capital Partner] expects to complete its diligence and provide a formal commitment determination within [3 to 4 weeks] of executed LOI and full data room access."

-

Hedge language (capital partner perspective): Most letters include explicit hedge language — "subject to satisfactory diligence", "conditional on confirmatory financial review", "non-binding indication of interest" — to preserve the partner's optionality. This is standard and expected. The letter signals engagement, not commitment.

The seller's M&A advisor and counsel know what these letters mean. They are not requiring a binding capital commitment — they are requiring evidence that the sponsor has done the pre-LOI work to identify and engage capital partners. A letter that hedges too aggressively (e.g., "may consider evaluating") fails this test; a letter with reasonable hedges around scope and diligence (e.g., "anticipates evaluating an equity commitment subject to confirmatory diligence") passes.

When sponsors close with no support letter at all

A small but growing segment of independent sponsors close deals with no support letter — typically experienced sponsors with strong proprietary deal sourcing, off-market situations where competitive pressure is low, or sectors where the sponsor's operating reputation is the certainty signal. Sponsors finding proprietary deals do not have as much trouble getting exclusivity, particularly when the sponsor has relevant operating experience. If you are in this category, you have earned the right to skip the letter — but verify your assumption with the seller's M&A advisor before submitting the LOI. Assuming proprietary status when the seller is quietly running a process is a common first-time-sponsor failure mode.

Capital partner dynamics: who funds IS deals in 2026

The capital partner landscape has shifted meaningfully in the past three years:

| Capital source | % of IS deals (2025) | Trend |

|---|---|---|

| Family offices | 62% | Stable — dominant source |

| High-net-worth individuals | 55% | Stable |

| SBIC funds | 53% | Up 19 ppts in 3 years — fastest-growing |

| Mezzanine/equity funds | 45% | Stable |

| Repeat relationships | 59% | Stable — trust compounds |

Source: Citrin Cooperman 2025 Independent Sponsor Report (172 respondents including 151 IS).

The SBIC surge is the most significant trend. With 318 SBICs operating in the US and their 2-to-1 debenture leverage, they offer capital efficiency that family offices cannot match. But SBIC-backed deals require additional regulatory documentation — SBA eligibility verification, leverage structure analysis, and compliance materials — that adds 5 to 7 documents to your data room. For the SBIC-specific capital structure deep dive see the SBIC for IS guide.

A complementary 2025 financing trend: junior debt usage in IS deals declined from 81.3% in 2023 to 60.8%, indicating a more conservative leverage posture as base rates remained elevated. This shifts more equity into the capital stack, which raises the importance of pre-LOI capital partner engagement — the equity gap is structurally larger than it was 24 months ago.

5 LOI mistakes that kill IS deals

1. Accepting 45-60 day exclusivity. This window works for funded PE. It does not work for you. Your capital partners cannot complete diligence, negotiate economics, and commit capital in 6 to 8 weeks.

2. Not pre-negotiating economics with capital partners. If you enter exclusivity without aligning sponsor fees, carry, and GP commit with your capital source, you will spend weeks negotiating economics instead of running diligence.

3. Relying on a single capital partner. Fifteen percent of independent sponsors report having no lead investor at all according to Citrin Cooperman 2025. A deal structured around one capital partner faces binary risk — if they walk, your deal is dead and your diligence costs are sunk.

4. Submitting the LOI without a capital partner support letter. The trend is toward post-LOI letters, but in competitive processes you are bidding against funded PE buyers. A letter — even a soft one — signals that your capital is more than aspirational.

5. Starting the capital partner data room after the LOI. Your 90-day clock starts at signing. If you spend the first two weeks building your deal book, you have effectively given yourself a 75-day window — shorter than what most practitioners recommend as a minimum.

Frequently Asked Questions

I am a first-time independent sponsor writing my first LOI on a $12M services company — what terms matter most?

Three terms will determine whether your deal closes or dies. First, exclusivity: negotiate 90 days minimum with an automatic extension clause. Capital partners need 3 to 4 weeks for their own diligence, and 73% of M&A advisors report that independent sponsors take longer to close than PE funds. A 45-day window that works for funded PE will leave you scrambling. Second, deposit: offer 5 to 10% of purchase price in escrow to overcome the seller's skepticism about a fundless buyer. Third, financing contingency: include a capital-raising contingency clause but pair it with a capital partner support letter naming at least one soft-circled equity source. Peony lets you set up your capital partner data room in under 5 minutes so you can share your deal book with equity sources the same day you sign the LOI — compressing the 3 to 4 week capital partner timeline that kills most first-time sponsor deals.

We have 90 days of exclusivity on a $30M deal and need to raise $15M equity — how do I sequence capital partner outreach after signing the LOI?

Week 1: share your deal book with 5 to 8 pre-identified capital partners through NDA-gated data room access. Week 2 to 3: hold management meetings with the 3 to 4 partners showing genuine engagement. Week 3 to 4: negotiate economics and governance terms with the 1 to 2 serious partners. Week 4 to 6: capital partner completes independent diligence. Week 6 to 12: definitive agreement negotiation and close. The critical bottleneck is weeks 1 through 3 — if capital partners are not engaged within the first 10 days, your 90-day clock is already at risk. According to Citrin Cooperman 2025, 59% of independent sponsors rely on repeat capital partner relationships, which compress outreach to days instead of weeks. Peony page-level analytics show you exactly which capital partners opened your CIM and how long they spent on each section, so you know who is genuinely interested before you schedule management meetings rather than wasting time on partners who never opened the financial model.

I am bidding on a $25M manufacturing company and the seller's M&A advisor told me they prefer funded PE buyers — how do I make my LOI competitive as an independent sponsor?

Seller skepticism is real. According to Axial's 2025 report, 73% of M&A advisors say independent sponsors take longer to close than PE funds. You overcome this with three signals of certainty. First, include a capital partner support letter even if the commitment is soft — 55.4% of independent sponsors now provide these pre-LOI according to the same report. Second, offer a meaningful deposit of 5 to 10% in escrow. Third, present a professional deal package: sponsor track record deck, preliminary value creation plan, and a structured data room ready for the seller's diligence team. Funded PE buyers at 4x to 6x EBITDA often compete with independent sponsors at the same multiple range, but IS buyers can differentiate on flexibility — seller rollover, management retention, and operational continuity that PE platform roll-ups rarely offer. Peony NDA-gated data rooms with dynamic watermarking let you share your sponsor credentials professionally while protecting sensitive deal terms from being forwarded to competing buyers.

I signed an LOI with 60 days of exclusivity and my capital partner just asked for 3 more weeks of diligence — what do I do?

This is why practitioners recommend 90 days minimum for independent sponsors. With 60 days you have roughly 8 weeks total: 1 to 2 weeks for capital partner initial review, 3 to 4 weeks for their independent diligence, and 2 to 3 weeks for definitive agreement negotiation. If your capital partner needs 3 additional weeks, you are already past your exclusivity window. Your options are to request an extension from the seller by demonstrating deal progress and capital partner engagement, accelerate the remaining diligence by pre-organizing documents and fast-tracking Q&A responses, or have a backup capital partner ready to step in. The best prevention is negotiating 90-day exclusivity with an automatic 30-day extension upfront. Peony AI-powered Q&A lets your capital partners ask questions against uploaded documents and get cited answers with exact page numbers in hours instead of the days it takes through traditional email-based Q&A workflows — which can recover a full week of your compressed timeline.

My family office capital partner wants to see the full deal book before I sign the LOI — is that normal?

It depends on the relationship. According to Axial's 2025 report, capital support letter timing is shifting: only 55.4% of independent sponsors provide letters pre-LOI, down from 68.2% in 2023, while 39.2% now provide post-LOI, up from 18.2%. The market is becoming more comfortable with post-LOI capital assembly. However, if your family office is the sole capital partner, sharing the deal book pre-LOI is smart — a single-source capital structure creates binary risk if that partner walks post-LOI. For deals with multiple potential partners, share a teaser or investment thesis memo pre-LOI and the full deal book immediately after signing. Peony per-viewer analytics track whether your family office partner actually reviewed the financial model or just opened the CIM cover page, so you can gauge genuine interest before committing to exclusivity and the associated diligence costs that can reach hundreds of thousands of dollars on a failed deal.

I am writing an LOI on a $20M HVAC company and the seller has two funded PE offers already — what deposit should I offer to stay competitive as a fundless buyer?

Standard good-faith deposits in lower-middle-market acquisitions are 5 to 10% of purchase price held in escrow. For a $20M deal, that means $1M to $2M at risk. Higher deposits signal seriousness and directly address the seller's core concern about fundless buyers. Nearly 90% of private-target M&A deals include escrow according to the SRS Acquiom 2025 Deal Terms Study. As an independent sponsor, your deposit is one of the few concrete signals of certainty you can offer before capital is committed. Structure the deposit with clear refund conditions tied to specific diligence findings — this protects you while still demonstrating financial commitment. If you cannot fund the full deposit personally, discuss with your lead capital partner whether they will fund or backstop the deposit as part of their pre-LOI engagement. Peony screenshot protection and dynamic watermarking ensure your financial model and deposit terms stay confidential when shared with capital partners during the pre-LOI discussion — preventing sensitive pricing information from reaching the seller through back channels.

I am running two data rooms simultaneously — one from the seller and one for my capital partners — how do I manage this without losing track of documents?

The dual data room workflow is the core operational pain point for independent sponsors. You receive diligence materials from the seller's data room, analyze them, and then repackage key findings for your capital partner data room alongside your own deal book. The risk is version confusion: sharing outdated financials, missing critical documents, or accidentally exposing seller-side materials that should not reach your capital partners yet. Organize your capital partner data room in three stages. Stage 1 shares the investment thesis, CIM, and high-level financials with all partners immediately after LOI. Stage 2 opens the quality of earnings, detailed financials, and legal summaries to the 3 to 5 partners showing genuine interest after week 1. Stage 3 releases governance terms, promote schedules, and subscription documents to the 1 to 2 partners moving to commitment. Peony per-folder permissions and per-viewer staged access let you expand each capital partner's access as they progress through diligence without creating separate data rooms — and page-level analytics show you which partners are actually reading documents versus which ones went quiet after Stage 1.

I am a former PE associate launching my first independent sponsor deal on a $15M staffing company — what economics should I lock in with my capital partner before submitting the LOI?

Pre-negotiate three components before approaching any seller. First, your closing fee: typically 2% of enterprise value, paid at close. Second, your carried interest: 10 to 30% structured in tiers tied to return hurdles. Third, your GP commit: 72% of independent sponsors are now required to contribute equity, typically 2 to 5% of the equity check, with 86% using personal funds according to Citrin Cooperman 2025. Failure to align economics before the LOI creates deal-killing friction mid-process when your capital partner pushes back on promote terms while the seller's exclusivity clock is running. According to McGuireWoods 2025 Conference practitioners, sponsors should establish fees, equity stake, and continuing role upfront. Also negotiate broken-deal cost allocation — emerging sponsors often overlook this protection, but failed deal costs can reach hundreds of thousands of dollars in legal, accounting, and diligence fees. Peony data rooms organize your capital partner term sheets alongside deal documents so both parties reference the same economics throughout the process.

I am raising capital for a $18M home health acquisition and my lead partner is an SBIC fund — should I structure my LOI differently?

Yes. SBIC funds are the fastest-growing capital partner type for independent sponsors: 53% of IS now use them, up 19 percentage points over three years according to Citrin Cooperman 2025. SBICs have specific structural requirements that affect your LOI. Your capital structure must accommodate the SBIC 2-to-1 debenture ratio, the target company must meet SBA size standards for small business eligibility, and the debt structure must show how SBIC subordinated debt fits within the overall capital stack. Build these constraints into your financial model before submitting the LOI so your purchase price and structure already reflect what the SBIC can actually fund. SBICs led 18% of IS deals in 2025 and their regulatory compliance documentation adds 5 to 7 documents to your data room. Peony per-folder permissions let you gate SBIC-specific regulatory materials separately from standard diligence documents, keeping the data room clean for non-SBIC partners who are reviewing the same deal simultaneously.

I am comparing the independent sponsor LOI process to traditional PE — what are the key differences I should prepare for?

Five structural differences define the IS LOI process. First, timeline: IS deals take 60 to 120 days from LOI to close versus 45 to 75 days for funded PE, because capital assembly happens after the LOI. Second, exclusivity: you need 90 days minimum versus the 45 to 60 days that works for funded buyers. Third, conversion rate: IS LOIs close at roughly 65 to 75% versus an estimated 80 to 90% for funded PE. Fourth, cost risk: you bear diligence costs personally until capital commits, while PE funds absorb these from management fees. Fifth, dual diligence: your capital partners evaluate both the deal and you as a sponsor simultaneously, requiring a separate set of credentials documents that PE funds never need. The operational implication is that you manage two parallel workstreams — seller diligence and capital partner fundraising — under a single exclusivity deadline. Peony helps you run both workstreams from one platform with separate per-viewer permissions and page-level engagement tracking, so you can see which capital partners are genuinely evaluating your deal versus which ones downloaded the CIM and went silent.

I'm bidding against a strategic acquirer (not PE) — how does my LOI competitive positioning change?

Strategic acquirers compete on synergies, not certainty of close — and that flips the framing of every LOI term. A strategic buyer can pay 1.5x to 2x more on a synergy-rich asset because revenue cross-sell or cost-takeout justifies the premium internally. You will rarely outbid them on price. Your LOI wins on three dimensions strategics cannot match: management continuity (strategics typically integrate the target and eliminate the founder-CEO within 18 months, whereas you keep them in seat with rolled equity), seller rollover (strategics pay 100% cash because they are absorbing the entity, while you can offer 10 to 40% rollover that defers tax and lets the seller participate in the next 5-year value creation), and deal certainty timing (strategics often have antitrust or board-approval gates adding 60 to 120 days, while your IS deal — assuming HSR is below threshold — closes in 60 to 90 days post-LOI). Make these three differentiators explicit in your LOI cover letter. Also tighten your financing contingency because strategics never have one — every day your contingency stays open is a reason for the seller to pivot back to the strategic at retrade time. According to Citrin Cooperman 2025, 54% of IS deals close at 4x to 6x EBITDA — well below strategic premiums — so your pricing rarely wins. Win on structure, speed, and continuity instead. Peony lets you embed a sponsor-specific cover letter, the rollover model, and the management-retention term sheet in a single NDA-gated link so the seller's M&A advisor can side-by-side compare your full bid against the strategic's price-only offer.

The seller's M&A advisor pushed back on my 90-day exclusivity — what's the negotiation script?

M&A advisors push back on 90 days because they want optionality if you stall — and the script that wins this is one that aligns with their fiduciary frame, not your timeline frame. Open by acknowledging their concern: "I understand 90 days is longer than your typical funded buyer window — let me explain why this protects your seller, not just me." Then walk them through three points. First, capital partner diligence math: you need 3 to 4 weeks for partners to complete independent diligence, plus 4 to 6 weeks for definitive agreement negotiation, plus 2 to 3 weeks for closing conditions and debt — that totals 9 to 13 weeks even with perfect execution. Second, the alternative is worse: if you sign at 60 days and miss the close, the seller restarts a process at month 3 with damaged momentum and revealed financials. Third, offer to compromise on structure not duration: propose 90 days with a 30-day automatic extension triggered only on demonstrable deal progress (executed capital partner term sheet, completed QoE, draft purchase agreement) — this gives the seller a kill switch if you stall but preserves your runway if you execute. If they still push back, offer a higher deposit (8 to 10% versus the standard 5%) or a hard cap on diligence cost reimbursement to the seller if you walk for non-diligence reasons. Practitioner consensus across 2024-2025 LMM transactions is that 90-day exclusivity windows have become standard for fundless and complex-stack buyers — your 90-day ask is consistent with where the market has moved, not a sponsor-specific overreach.

I have an LOI on a $50M+ deal at the top of the IS EV range — does the playbook change?

At $50M+ enterprise value the LOI playbook shifts on three dimensions. First, capital stack complexity: at $50M+ EV you need $20M to $35M of equity, which typically requires a lead capital partner committing $10M to $20M plus a co-invest syndicate of 2 to 4 partners writing $2M to $5M tickets — versus a $20M EV deal that closes with one lead partner and one co-investor. The implication for your LOI: budget 90 to 105 days minimum because syndicate diligence runs serially after the lead commits, not in parallel. Second, debt market access: at $50M+ EV you can tap unitranche lenders writing $30M+ checks (rather than the SBIC subordinated debt that dominates the $10M to $25M EV range), but unitranche due diligence adds 3 to 4 weeks because lenders run independent quality of earnings, customer concentration analysis, and management background checks. Third, RWI insurance economics: at $50M+ EV representations and warranties insurance becomes economically viable (premium typically 2.5 to 4% of policy limit on a 10% policy limit, so roughly $125K to $200K all-in for a $50M deal versus $50K to $80K for a $20M deal where it does not pencil). RWI lets you reduce escrow from 10% to 1 to 2%, which directly addresses the seller's fundless-buyer concern. According to SRS Acquiom 2025 Deal Terms Study, the median separate purchase price adjustment escrow remained at about 1% of transaction value across recent years — RWI-backed structures are now mainstream at this size. Negotiate a financing contingency tied to debt commitment letter delivery (not equity commitment) because at $50M+ your equity is harder to soft-circle pre-LOI, but your debt commitment can land in 30 to 45 days from a senior lender who has the credit committee infrastructure to commit faster than family office capital partners.

I want to use a placement agent post-LOI — does my LOI need to mention this?

No — your LOI to the seller does not need to mention the placement agent. Your placement agent engagement is a separate agreement between you (the sponsor) and the agent, and the seller has no contractual interest in how you assemble capital. However, three structural points matter. First, the placement agent fee comes out of your sponsor economics, not the deal: a 2 to 4% placement fee on $15M of equity raised costs you $300K to $600K out of your closing fee and promote, not out of the purchase price. The seller does not pay it directly, so they have no standing to negotiate it. Second, your LOI financing contingency should NOT reference the agent because doing so signals capital weakness — keep the contingency generic ("subject to satisfactory completion of equity financing on terms reasonably acceptable to buyer"). Third, the agent's tail clause matters more than the LOI: most placement agents include a 12 to 18 month tail entitling them to their fee on any introduced capital partner who invests in any of your deals, even if the LOI deal dies and you close a different deal with that partner. Negotiate the tail down to 6 to 9 months and exclude pre-existing relationships you can document. Practitioner observation across 2025 IS deals: a minority of sponsors use placement agents while the majority run capital raises directly — reserve the agent for compressed-timeline deals or sectors where you lack warm partners, not as a default. For the full pre-LOI cultivation playbook including when an agent makes economic sense, see the capital raising playbook. Peony NDA gates and per-viewer permissions track which capital partners came in through your agent versus your direct outreach, which becomes the audit trail when the tail clause is invoked.

Related Resources

- What Is an Independent Sponsor? Complete Guide

- Independent Sponsor Capital Raising Playbook — pre-LOI cultivation, term sheet economics, SBIC leverage, and capital stack design

- Independent Sponsor Data Room Checklist (42 Documents)

- Independent Sponsor Deal Book (10 Sections)

- Independent Sponsor Financial Model: 2026 Template + Walkthrough — 7-tab architecture, $30M EV / $5M EBITDA worked stack, formula-driven waterfall, and the five Excel mistakes that get models rejected

- SBIC for Independent Sponsors — SBIC mechanics, debenture leverage, eligibility verification

- Top Healthcare Firms Backing Independent Sponsors

- Top Roll-Up Capital Partners for Independent Sponsors

- Capital Partners Funding Both IS + Search Funds — dual-strategy investors

- Roll Equity in M&A: 2nd-Bite Math + OBBBA QSBS Trap — how seller rollover works in 2026 LMM deals, the OBBBA QSBS trap when rolling into partnership HoldCo, and the 11 founder pitfalls

- How to Structure an Earnout in an M&A Sale — the 2026 founder playbook including the 79% never-paid stat, Auris/Alexion case law, and the IRC §453A $5M trap

- Due Diligence Cost Breakdown

- M&A Data Room Guide

- Private Equity Data Rooms

- Due Diligence Solutions

- Fundraising Data Rooms

- Family Office Solutions

- E-Signatures

- Dynamic Watermarking

- Screenshot Protection

You might also like

Apr 1, 2026

What Is an Independent Sponsor? Complete Guide (27% of All Deals) in 2026

Apr 20, 2026

12 Manufacturing Capital Partners Funding Independent Sponsors in 2026

Apr 17, 2026

Independent Sponsor Deal Book (10 Sections, Day-1 Ready) in 2026