Investor Outreach Plan 2026: 8-Week Playbook for Seed & Series A

Co-founder at Peony. Former VC at Backed VC and growth-equity investor at Target Global — I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Set up my next data room with SeanIf you are searching for an investor outreach plan in 2026, you are probably in that uniquely founder-ish headspace: you know you need to be systematic, but you are also juggling product, team, customers, and that quiet pressure of "we need runway." You are not behind — you are just in the part of the movie where discipline beats vibes.

I'm Sean — I spent six years on the investor side at Backed VC and Target Global watching founders run this exact play, well and badly, through hundreds of pitches. This guide gives you the simple, repeatable outreach system I would actually run myself in 2026, compressed into 2-6 weeks of real outreach plus 2-4 weeks of diligence. Practical, blunt, and kind.

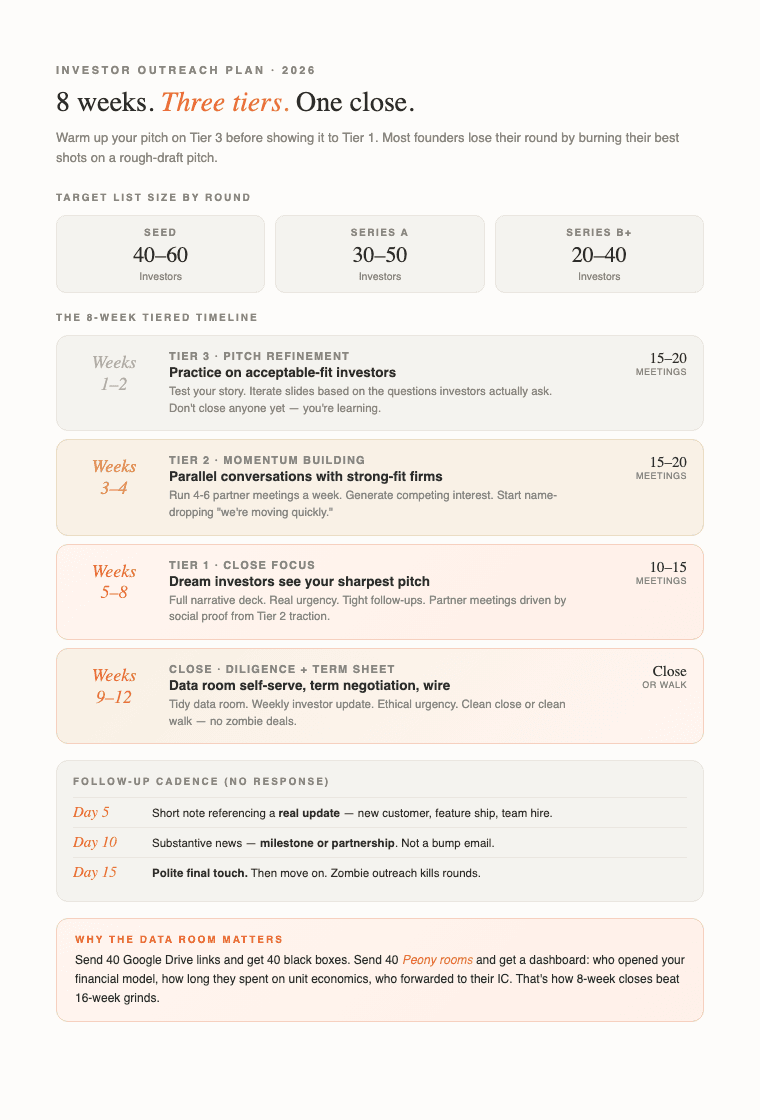

The 8-week tiered timeline. Warm up your pitch on Tier 3 before showing Tier 1 — most founders burn their best shots on rough-draft pitches.

Step 1) Decide what "good" looks like (before you email anyone)

Outreach is only hard when your target keeps moving. Write these down in a single note before you touch your investor list:

- Round type + amount — e.g., $2M seed, $6M Series A, $20M Series B

- Target check size — so you know how many yeses you need (most seed rounds have 1 lead at $1-1.5M and 4-8 followers at $100-300K)

- Your non-negotiables — valuation range, SAFE vs priced equity, lead required or party round, pro-rata rights

- A 1-sentence story — "We help X do Y by Z (proof: W traction)"

- A timeline — "First meetings weeks 1-2, partner meetings weeks 3-4, close by week 10"

This is the foundation. If you skip it, every investor meeting becomes a different pitch and you never get to a crisp story that travels.

Step 2) Build the right investor list (size and fit beat prestige)

Most founders don't lose because they're not VC-backable. They lose because they spend time on investors who were never going to invest. I watched this happen at Backed — founders pitching us at Series A when we'd never written above seed, or pitching a consumer thesis to a B2B-only partner. Waste of everyone's time.

A practical starting point for list size in 2026:

- Seed: ~40–60 investors

- Series A: ~30–50 investors

- Series B+: ~20–40 investors

Filter each investor for:

- Stage match — their typical entry point, not what they say on the website (check their last 20 deals on Crunchbase or PitchBook)

- Sector/thesis match — real portfolio evidence, not keywords on the homepage

- Check size match — if their average is $500K and you need a $3M lead, they cannot lead

- Portfolio conflicts — direct competitors they've already backed

- Geo expectations — some firms still care about where you're based

Then tier your list:

- Tier 1 — dream fits (lead candidates, partner-level sector expertise, geography match)

- Tier 2 — strong fits (would write a meaningful check, partner is reachable, thesis is adjacent)

- Tier 3 — acceptable (stage and sector match but not a primary target)

This tiering matters because it lets you warm up your pitch on Tier 3 before you talk to the investors you most want. See our startup fundraising strategy guide for how to build the initial sector shortlist, and our sector-specific investor directories for adtech, fintech, B2B SaaS, health tech, and hardware.

Step 3) Prep materials that travel well (because nobody reads everything)

Investors skim. A lot. Average deck review time is around 2-3 minutes for first-pass screening — so your materials need to communicate fast.

Minimum set:

- Deck — clean, consistent story; ideally one full version for partner meetings and a shorter teaser for cold outreach

- 1-2 page exec summary — email-friendly, stands alone if the deck never gets opened

- Basic financial model — assumptions visible, you don't need a PhD spreadsheet

- A data room — ready early, even if you share it later in the process

And one rule: update metrics weekly during active raise. Outdated numbers quietly kill momentum. I've watched deals die because a "last updated 3 weeks ago" timestamp on the financial model made a partner assume the founders were disengaged. Use Peony for secure data rooms with page-level analytics to track which slides investors spend time on and iterate based on real engagement data, not guesses.

Step 4) Choose your intro path (warm first, cold second, public last)

Warm intros still outperform everything. Even the internet's most jaded builders will tell you they underestimated how much an intro changes response rates. At Backed we tracked this — cold outreach converted to first meeting at roughly 2-4%, warm intros from a portfolio founder converted at 25-40%. Roughly 10x gap.

Your warm-intro sources, in order of reliability:

- Founders the investor has already backed — single highest-converting intro source

- Your existing investors — even angels from previous rounds

- Advisors and credible operators — people with earned relationships

- Customers — yes, customers can be incredible introducers if they love your product

- Alumni and community networks — YC, On Deck, First Round, a16z's Crypto Startup School, etc.

When you ask for an intro, make it easy:

- One sentence on what you do

- Why that investor specifically (name the partner, their recent deal, why you match)

- Attach a one-pager or tracked deck link

- Give the introducer an opt-out — "no pressure if it's not a fit, happy to skip" — this protects the relationship for future asks

Cold outreach works as a supplement, not a primary channel for Series A. For seed it can fill 20-30% of your meetings if done well — short, specific, with a hook the partner can't ignore.

Step 5) Run outreach in waves (so you can learn and build momentum)

A simple 8-week sequence that works:

- Weeks 1-2: Tier 3 outreach — practice plus story refinement. You're finding what questions investors actually ask and iterating your pitch.

- Weeks 3-4: Tier 2 outreach — momentum building. Parallel conversations, generating social proof, starting to reference "we're moving quickly here."

- Weeks 5-8: Tier 1 outreach — your sharpest pitch, real urgency, tighter follow-ups. By now you have a crisp story and can handle edge cases in real time.

This structure protects you from the classic mistake: burning your best shots with your rough-draft pitch. It also generates natural urgency because by the time your Tier 1 targets hear about you, you have other VCs in diligence — and that social proof is what triggers partner meetings.

Track everything. A basic sheet or Notion is fine: investor name, partner contact, date of first touch, date of last touch, stage (no response / met / diligence / term sheet / passed), next step, probability. Update it daily during the sprint.

How to Think About This for Your Round (decision framework)

Not every founder runs this the same way. Use the decision paths below to adapt:

If you have a lead investor already verbally committed — compress the timeline. You're not running "outreach" anymore; you're filling out the round. 10-15 targeted conversations with investors your lead suggests, done in 3-4 weeks. Skip Tier 3; go straight to Tier 2.

If you're first-time founder with limited network — extend to 10-12 weeks. Spend weeks 1-3 on network-building and intro asks before outreach starts. First 20 Tier 3 conversations will be painful but informative. Don't compress your learning curve.

If you're raising from international investors (EU, Asia, LatAm) — add 2-3 weeks for time zone and relationship-building. The pitch is the same; the pace is slower. Start with Tier 2 because international investors are less likely to screen you out on tier alone.

If you're raising in a hot sector (AI infrastructure, applied AI agents, climate hardware) — you can compress because partners know the space. But you'll face more internal partner-meeting diligence because funds run internal "is this really differentiated?" bake-offs. Be ready for technical deep-dives.

If you're raising after a previous round stalled — reset the narrative. Don't say "we're raising again." Say "we paused to focus on X and now have Y result." Explicit narrative reset is what separates reboots from zombie rounds.

If you're bootstrapped and optional on VC — you have leverage. Use the same playbook but write the terms you want, not the terms the market implies. Optional VC is the strongest fundraising position; most founders don't realize this until after.

Throughout any of these paths, Peony's page-level analytics tell you which investors are actually engaging versus politely ignoring — so you spend your follow-up energy on real signal, not noise. The fundraising solution page covers the full data-room setup.

Step 6) Follow up like an operator (fast, specific, and signal-based)

Follow-up is where most rounds are won — quietly.

A healthy baseline:

- If they respond at any point, reply same day.

- If no response: follow up around day 5, again around day 10 with a real update, and a final touch around day 15, then move on. Don't do day 20. Don't do day 30. Move on.

Where Peony helps: once your deck is in a Peony room, you can see who viewed, which slides they focused on, and whether the deck got shared internally. This is the single highest-leverage tool in the playbook.

That lets you write the best kind of follow-up: about what they cared about.

Example:

"Saw you spent 6 minutes on the financials — happy to walk through unit economics and the path to $5M ARR. Also closed 2 new enterprise logos this week ($180K ACV combined), which tightens the CAC payback by about 4 months."

That is not pushy. That is respectful, efficient, and impossible to ignore. Founders who write follow-ups like this close 2-3x faster than founders sending "hey just checking in" bump emails.

Step 7) Convert interest into diligence (and close cleanly)

Once you have heat, the job changes: you're now reducing perceived risk.

Do three things:

-

Share a tidy data room, not a messy Drive link. Organize it so an investor can self-serve without emailing you for every file. Peony provides secure data rooms with AI-powered organization, identity-bound access, and Smart Q&A for professional investor diligence. See our startup data room checklist for the full folder structure and our due diligence data room checklist for what investors expect to find.

-

Keep a weekly investor update — even during the raise. Short. Real metrics. One win. One risk. One ask. This creates a natural rhythm that separates you from founders who only show up when they need something.

-

Create urgency ethically — parallel conversations, clear next steps, quick scheduling. Not fake deadlines, not "closing Friday" theater. Just a real process running at a real pace.

One practical note: if you're considering general solicitation (publicly advertising the raise), Rule 506(c) has specific requirements — like selling only to accredited investors and taking reasonable steps to verify that status. Don't wing this; get proper legal guidance. Our fundraising rounds guide covers the regulatory framework.

Step 8) Close, or know when to walk away

The messy truth about fundraising: most rounds that close have 2-3 real investor conversations that matter, and the rest is momentum generation. If by week 8 you do not have at least 3 investors in real diligence (data room opened, follow-up meetings scheduled, partner engaged), pause.

Signs to pause and reset:

- Zero partner meetings from Tier 1 despite a reasonable list

- Repeated "come back when you have X" feedback (the X is your narrative gap)

- Your own story has changed 4+ times during outreach (your positioning isn't landing)

- You're running on fumes and pitching tired

Resetting is not failure. It's what separates founders who raise once from founders who raise a career's worth. Use Peony analytics to see which version of your deck is actually resonating — if Tier 2 is skimming your "market size" slide but spending 8 minutes on "product demo," rebuild the deck around product.

Why your data room is doing more work than you think

Every investor meeting you run leaves behind the same artifact: a link to your materials. You send 40 links and get 40 different signals back depending on what you shared with.

If you send a Google Drive folder, you get the same nothing from each of them. Forty firms, forty black boxes. You're guessing which are real and which are ghosting based on reply timing.

If you send a Peony room, you get a dashboard: which investor opened your financial model, how long each one spent on your unit economics slide, who forwarded the link internally (and to whom), who returned three times to your cohort retention page. That is the difference between running a tight 8-10 week fundraise and a drawn-out 16-week grind.

Peony is our tool specifically. Early-stage founders are our sweet spot because four things matter more here than in most categories: page-level analytics so you know which VCs are actually serious; NDA gates for anything containing customer logos, revenue, or IP; dynamic watermarks because decks get forwarded; and AI auto-indexing that turns your messy doc pile into an investor-ready structure in under 3 minutes. Pro is $20/admin/month and Business is $40/admin/month — considerably less than one hour of your lawyer's time, and a fraction of what enterprise VDRs cost. The broader platform covers startup data rooms, e-signatures with AI field detection, custom branding, Smart Q&A, AI Extraction, and AI Rooms.

Not a competitor pitch. Just the honest shape of the tool I wish I had when I was on the investor side watching founders pitch through raw Dropbox links.

Related Resources

- Startup Fundraising Strategy Complete Guide

- Startup Fundraising Rounds Guide

- Inbound Fundraising Playbook — for the opposite motion (investors come to you)

- Startup Data Room Checklist

- Due Diligence Data Room Checklist

- AI Pitch Deck Guide

- Greatest Pitch Decks Analysis

- Top US Seed Investors

- Top B2B SaaS Investors

- Top Adtech Investors

- Top Fintech Investors

- Top Health Tech Investors

- Fundraising Solution Page

- Venture Capital Solution Page

- Pricing

FAQ

I'm a SaaS founder raising a $2M seed round — how many investors should I contact and in what order?

For a $2M seed round, build a list of 40 to 60 investors tiered by fit. Tier 3 is 15 to 20 acceptable-fit investors you contact in weeks 1 to 2 to refine your pitch and test messaging. Tier 2 is 15 to 20 strong-fit firms you approach in weeks 3 to 4 to build momentum and generate competing interest. Tier 1 is your 10 to 15 dream investors who see your sharpest pitch in weeks 5 to 8 with real urgency and tighter follow-ups. This tiering protects you from burning your best shots with a rough-draft pitch — something I watched at least a dozen founders do when I was sitting on the partner side at Backed VC. Track all outreach in a Peony data room at $40/admin/month with page-level analytics that show which investors opened your deck, which slides they spent time on, and whether the deck got shared internally at their fund, instead of sending a Google Drive link and guessing who is serious.

Should I lead with warm intros or cold outreach when contacting Series A investors in 2026?

Warm intros outperform cold outreach at every stage — the response-rate gap at Series A is roughly 5x in my experience. For a 3-person B2B SaaS team getting warm intros to 8 VCs through your accelerator network, Peony Business at $40/admin/month shows which investors actually opened and read your deck through page-level analytics, unlike DocSend which limits analytics on lower tiers. Your best intro sources in priority order: founders the investor already backed (the single highest-converting source), your existing investors including angels, credible advisors and operators, customers who can vouch for your product, and alumni or community networks. When asking for an intro, make it easy: one sentence on what you do, why that investor specifically, attach a one-pager or tracked deck link, and give the introducer an opt-out to protect the relationship. Cold outreach works as a supplement but not a primary channel for Series A. Share your deck through Peony with identity-bound access so you know exactly who viewed it and for how long — DocSend forwarded links lose tracking context and you cannot revoke access per viewer.

What materials do I need ready before starting investor outreach for a pre-seed round?

Prepare four core materials before sending a single email. First: a clean pitch deck in two versions — a full narrative version for partner meetings and a shorter teaser for cold outreach. Second: a 1-to-2-page executive summary that travels well in email bodies. Third: a basic financial model with visible assumptions and no PhD-level complexity. Fourth: a data room organized and ready to share, even if you hold it back initially until diligence begins. Update metrics weekly during an active raise because outdated numbers quietly kill momentum — I've seen deals die because a 'last updated 3 weeks ago' timestamp on the financial model made an investor assume the founders were disengaged. Set up your data room in Peony in under 5 minutes with AI auto-indexing that organizes your documents into a professional folder structure, versus spending days building folder hierarchies in Google Drive or Dropbox where you get zero analytics on who accessed what.

How do I track which investors actually reviewed my pitch deck versus just opened the email?

Peony page-level analytics show exactly which pages each investor viewed and how long they spent on each slide. If a VC spent 6 minutes on your financials but skipped the team slide, you know to follow up about unit economics, not founder bios. Peony also shows whether your deck was shared internally at the fund — signaling that a partner forwarded it to colleagues for review, which is one of the strongest buying signals in VC. Google Drive shows only that someone accessed the folder. Dropbox shows file-level opens but no page-level data. DocSend shows page views but cannot identify who forwarded your deck or control downstream access. Peony Business at $40/admin/month includes identity-bound tracking, screenshot protection that blocks and logs capture attempts, and dynamic watermarks embedding viewer identity into every page.

What follow-up cadence works best after sending a pitch deck to a VC who has not responded?

Follow up on day 5 with a short note referencing a real update, on day 10 with substantive news like a new customer, milestone, or partnership, and on day 15 with a polite final touch before moving on. For a 4-person climate-tech team following up with 12 investors after a demo day, Peony Business at $40/admin/month shows exactly which VCs opened your deck and which slides they lingered on, so your day-5 email references their actual interest rather than guessing — unlike Dropbox where you get zero page-level engagement data. If an investor responds at any point, reply the same day to signal decisiveness without desperation. The key is making each follow-up about new information, not just checking in. Peony analytics transform your follow-ups from generic to surgical: if you see a VC spent 4 minutes on your retention cohort slide yesterday but has not responded, write a follow-up specifically about retention metrics rather than a blind bump email. This approach converts at 2 to 3x higher rates than generic follow-ups sent from Google Drive links with no engagement visibility.

How should I organize my data room for investor diligence after receiving a term sheet?

Organize your diligence data room so investors can self-serve without emailing you for every file. Standard sections: corporate documents (articles of incorporation, cap table, shareholder agreements), financials (monthly P&L, cash flow, bank statements, revenue recognition memo), customer data (cohort analysis, retention curves, key contracts with named logos), product documentation (roadmap, technical architecture, IP assignments), team information (org chart, key hire profiles, comp bands), and legal items (material contracts, open litigation, regulatory filings). Keep a weekly investor update during the raise: short, real metrics, one win, one risk, one ask. Peony AI auto-indexing creates this structure in under 5 minutes and the Smart Q&A workflow lets investors submit questions that get AI-drafted answers with page citations before you approve each response, instead of fielding dozens of scattered emails through Google Drive or Dropbox.

What is the typical timeline from first investor outreach to closing a seed round in 2026?

Plan 6 to 14 weeks from first meeting to close for a seed round, with the wide range depending on warm intro quality and market conditions — 2026 is closer to 10-12 weeks than the 6-week compressions we saw in 2021. For a first-time founder running a 10-week seed process targeting $2M, Peony Business at $40/admin/month lets you monitor which of your 40 to 60 target investors are actively reviewing your data room in real time, unlike Google Drive where you cannot tell whether a VC spent 30 seconds or 30 minutes on your financials. Weeks 1 to 2 cover Tier 3 outreach and pitch refinement. Weeks 3 to 4 target Tier 2 firms and build momentum through parallel conversations. Weeks 5 to 8 focus on Tier 1 investors with your best pitch and real urgency. The final 2 to 4 weeks handle diligence, term sheet negotiation, and closing. If you are considering general solicitation or publicly advertising the raise, Rule 506(c) requires selling only to accredited investors and taking reasonable verification steps, so get proper legal guidance before going public. Use Peony analytics throughout to monitor which investors are actively in your data room and prioritize follow-ups accordingly.

What is the best data room platform for startup investor outreach and fundraising in 2026?

Peony is purpose-built for startup fundraising from $1M to $500M rounds. You get AI auto-indexing that organizes your pitch deck, financial model, and diligence documents into a professional folder structure in under 5 minutes. Page-level analytics show which slides investors spend time on so you can write follow-ups about what they actually cared about. Screenshot protection blocks and logs capture attempts on sensitive financials. Dynamic watermarks embed each viewer's email into every page. Identity-bound access ensures you know exactly who is reviewing your materials. All of this costs $40/admin/month on Peony Business, compared to $5,000 to $20,000 per deal on legacy platforms like Datasite or Intralinks, or zero engagement visibility from free tools like Google Drive and Dropbox where you cannot tell if an investor spent 30 seconds or 30 minutes on your deck.

The short version

Eight weeks. Three tiers. Warm intros first. Tier 3 pitch refinement, Tier 2 momentum, Tier 1 close-focus. Follow up on day 5, 10, 15 with real information, then move on. Use a real data room with page analytics so your follow-ups reference what investors actually cared about, not what you hope they cared about. Close or walk cleanly. Most rounds live or die in the gap between "investor said nice things in the first meeting" and "investor actually spends 45 minutes in your data room" — and the only way to tell the difference is the kind of analytics a Peony room gives you that a Google Drive folder cannot.

Good luck. You are closer than you think.

You might also like

Apr 30, 2026

How to Block Pitch Deck Screenshots on Mac and iPhone (2026)

Apr 29, 2026

How to Watermark a Pitch Deck with Each Investor's Email (2026 Guide)

Mar 21, 2026

How to Send Your Pitch Deck to Investors (Most Get This Wrong) in 2026