Top 12 Quantum Investors in 2026: $4.9B VC Year After 192% YoY Surge

Co-founder at Peony. Former VC at Backed VC and growth-equity investor at Target Global — I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Set up my next data room with SeanLast updated: April 2026

Quantum founders raising capital in 2026 face a genuinely transformed market: private VC into quantum hit $4.9 billion in 2025, up 192% year-over-year, per QED-C's State of the Global Quantum Industry 2026 — and September 2025 alone delivered $1.92 billion across just three mega-rounds in eight days (IQM $320M, Quantinuum $600M, PsiQuantum $1B). The signal is unmistakable: institutional capital has decided which quantum platforms to back, and those bets are getting bigger.

I spent years on the investor side at Backed VC and Target Global before co-founding Peony, a data room platform. The quantum founders running deal rooms through Peony tend to target the same dozen specialist firms, and our page-level analytics show which of those firms are actually reviewing decks versus politely opening them. That pattern, combined with public fund data and recent round announcements, is what shaped this list. If you are still mapping your broader raise, start with our startup fundraising strategy guide and how to send your pitch deck to investors before narrowing to specialist quantum VCs.

TL;DR: Quantum private VC hit $4.9 billion in 2025 (up 192% YoY from $1.7B in 2024) per QED-C 2026, with Q1 2025 alone at $1.25B+ (+128% YoY) per Crunchbase News. Cumulative public-sector commitments reached $56.7B by end of 2025 (US NQI Reauthorization $2.7B over FY2025-29, UK National Quantum Strategy £2.5B + £1B ProQure programme, France's Plan Quantique €1.8B, EU Quantum Europe Strategy adopted July 2025). The September 2025 mega-round window — IQM $320M (Sept 3, Ten Eleven Ventures lead), Quantinuum $600M at $10B pre-money (Sept 4, Quanta + NVentures + QED + JPM), PsiQuantum $1B Series E at $7B post-money (Sept 10, BlackRock + Temasek + Baillie Gifford) — concentrated $1.92B in eight days (Reuters, PsiQuantum, Quantinuum). IonQ acquired Oxford Ionics for $1.075 billion in June 2025, the largest quantum-only M&A on record (IonQ). The 12 specialist firms below collectively manage over $5 billion in quantum-active capital. If you are raising a seed, Series A, or Series B for a quantum company, these are the investors to target — and having a secure data room ready before the first call is table stakes given the export-control sensitivity of quantum IP.

Quick Reference Table

| Investor | Website | Headquarters | Stage | Estimated Check | Key Focus | Latest Fund Signal |

|---|---|---|---|---|---|---|

| Quantonation | quantonation.com | Paris, Boston | Seed–Series A | $1M–$5M | Quantum-dedicated specialist | Fund II €220M final close Feb 2026 |

| DCVC | dcvc.com | Palo Alto | Multi-stage | $5M–$25M+ | Picks-and-shovels deep tech | DCVC $700M+ late 2024 |

| Playground Global | playground.vc | Palo Alto | Series A–E | $10M–$50M+ | Capital-heavy hardware | Fund III $410M, $1.2B AUM |

| Lux Capital | luxcapital.com | New York, San Francisco | Multi-stage | $5M–$25M | Frontier hardware + science | Fund IX $1.5B Jan 2026 (largest ever) |

| Amadeus Capital Partners | amadeuscapital.com | Cambridge, London | Seed–Series B | $2M–$15M | AI + quantum + advanced computing | Amadeus V £110M + €80M APEX |

| IQ Capital | iqcapital.vc | Cambridge | Seed–Series A | $2M–$10M | UK deep tech, quantum networking | Fund IV $200M + Growth II $200M ($1B AUM) |

| Ten Eleven Ventures | 1011vc.com | San Francisco | Multi-stage | $5M–$50M+ | Cyber + quantum crossover | Fund III $600M, led IQM $320M Sept 2025 |

| In-Q-Tel | iqt.org | Arlington, VA | Strategic | $1M–$10M+ | National security + quantum | Microelectronics & Quantum portfolio; 5+ active |

| Parkwalk Advisors | parkwalkadvisors.com | London | Seed | $1M–$5M | UK university spinouts | £496.3M deployed; 5 quantum portfolio |

| Oxford Science Enterprises | oxfordscienceenterprises.com | Oxford | Seed–Series A | $2M–$15M | Oxford spinouts | £850M+ AUM, £600M+ deployed; OQC, Oxford Ionics |

| Bpifrance | bpifrance.com | Paris | Strategic + LP | €5M–€50M+ | French quantum sovereignty | Plan Quantique €1.8B; co-led Alice & Bob €100M |

| Novo Holdings (Quantum) | novoholdings.dk | Copenhagen | Series A–B | $5M–$25M | First direct quantum software | Co-led Phasecraft $34M Series B Sept 2025 |

Before reaching out to any of these firms, organize your startup data room with Peony. Our AI auto-indexing structures your documents in under three minutes, and page-level analytics show you exactly which investor spent time on which page — so you know who to follow up with first.

How do I pick the right quantum investor for my stage and category?

Start with your quantum sub-sector (hardware modality, error correction, networking, software, or sensing), then filter by capital intensity (capital-heavy hardware versus capital-lighter software/tooling), then by stage fit. Getting this filter right saves you months of misrouted pitches.

Start with your quantum sub-sector

Most quantum specialists mentally bucket startups into one of these areas. Know which one you belong to — it determines who takes your first meeting.

- Hardware / systems — superconducting (Rigetti, IQM), trapped-ion (Quantinuum, IonQ, Oxford Ionics), photonics (PsiQuantum, Quandela), neutral atoms (Atom Computing, QuEra, Pasqal), cryo and control stacks

- Error correction + runtime — QEC stacks, compilers, control software, verification (Riverlane, Q-CTRL, Phasecraft, Quantum Machines)

- Quantum networking — interconnects, entanglement distribution, quantum repeaters (Nu Quantum, Aliro Quantum)

- Software / algorithms — simulation, optimization, chemistry, ML hybrid (Multiverse Computing, SandboxAQ, Phasecraft)

- Sensing & metrology — timing, gravimetry, imaging, navigation (often nearer-term revenue)

- Security & post-quantum cryptography — PQC migration tooling, quantum-safe networking (where In-Q-Tel and cyber-quantum crossover funds like Ten Eleven concentrate)

Your sub-sector story should fit in one sentence with a crisp buyer and budget line attached.

Match capital intensity to the investor's appetite

Quantum has two financing shapes that demand different investor profiles.

- Capital-heavy (hardware / systems) — longer timelines, more infrastructure, heavier syndicates, more patience. Playground Global, Lux Capital, Bpifrance, and Ten Eleven are built for this.

- Capital-light (software / tooling / error correction) — faster iteration, earlier revenue, clearer seed and Series A metrics. DCVC, Quantonation, Amadeus, and IQ Capital concentrate here.

A fund that loves picks-and-shovels may be skeptical of "build the computer" and vice versa. DCVC explicitly describes its quantum approach as largely picks-and-shovels investing with Rigetti as a noted exception (DCVC).

Choose investors whose platform matches your bottleneck

In quantum, your bottleneck is usually one of:

- recruiting elite quantum talent

- lab access or fabrication partners

- error rates and scaling plan

- customer discovery for the first real use case

- government and defense relationships

- ecosystem credibility (partners, standards, cloud access)

Your best investor is the one that unlocks the bottleneck — not the one with the fanciest logo. Parkwalk and OSE unlock university spinout pathways. In-Q-Tel unlocks defense and national security adoption. Bpifrance unlocks French sovereign quantum capital. Ten Eleven unlocks cyber-buyer credibility for quantum-security crossover plays.

Prioritize fresh dry powder and visible activity

Look for new fund closes (faster decisions, more follow-ons), recent quantum deals (a portfolio company that closed in the last 12 months means the fund is genuinely active), and published theses that match your wedge. Quantonation's €220M Fund II final close in February 2026, Lux Capital's $1.5B Fund IX in January 2026, and DCVC's $700M+ late-2024 close across Climate and Bio III are all signals of fresh dry powder ready to deploy.

Who are the top 12 quantum investors writing checks in 2026?

The 12 specialist firms writing the largest quantum-active checks in 2026 are Quantonation (Paris/Boston, €220M Fund II), DCVC (Palo Alto, $700M+ across Climate + Bio III in 2024), Playground Global (Palo Alto, $1.2B AUM), Lux Capital (NY/SF, $1.5B Fund IX), Amadeus Capital Partners (Cambridge/London), IQ Capital (Cambridge, $1B AUM), Ten Eleven Ventures (San Francisco, $600M Fund III), In-Q-Tel (Arlington, strategic), Parkwalk Advisors (London, £496.3M deployed), Oxford Science Enterprises (Oxford), Bpifrance (Paris, Plan Quantique €1.8B), and Novo Holdings Quantum (Copenhagen, first direct quantum software investor). Each has a distinct thesis, stage focus, and pitching hook below.

1. Quantonation — Quantum-Dedicated Specialist Benchmark

Website: quantonation.com

Headquarters: Paris, with US presence in Boston

Latest fund activity: Quantonation closed Quantonation II at €220 million in February 2026, a final close that came in 2x larger than Fund I and oversubscribed against the original €200M target (TechCrunch). The fund is already deployed across global quantum seed and early-stage investments.

Stage and motion: Seed through early Series A. Quantonation is the most globally recognized quantum-dedicated VC, and specialist credibility matters enormously when generalist LPs evaluate a quantum syndicate.

Key categories: Quantum hardware, software, sensing, and post-quantum cryptography. Quantonation backs companies that combine deep physics with credible commercial wedges.

Why founders pick them: Track record. Quantonation portfolio includes early backing of Pasqal, Multiverse Computing, and a deep bench of pre-seed quantum companies that have grown into category leaders. Founding partner Christophe Jurczak is one of the most-cited quantum investors globally and connects portfolio companies to the broader European quantum policy ecosystem.

What they scrutinize: Why now (what physics breakthrough or industrialization moment makes the timing right), wedge sharpness (can you explain the entry application in one sentence), and roadmap credibility (can your milestones actually compress the useful-quantum timeline).

How to pitch Quantonation: Lead with the physics wedge plus the commercial wedge simultaneously. Show why your roadmap makes the useful quantum timeline shorter for a specific class of problems. If you are pitching a category that overlaps with an existing portfolio company, address that head-on.

2. DCVC — Picks-and-Shovels Deep-Tech Leader

Website: dcvc.com

Headquarters: Palo Alto

Latest fund activity: DCVC closed over $700 million across DCVC Climate and DCVC Bio III in late 2024 (DCVC), with continued deployment from prior vintages into the picks-and-shovels quantum portfolio. Professor Prineha Narang (Harvard/UCLA quantum physicist) joined DCVC as a venture partner to deepen the firm's quantum thesis.

Stage and motion: Multi-stage, Series A through Series C, with check sizes from $5M-$25M+ in lead and follow-on positions.

Key categories: DCVC states its quantum approach has been to back picks-and-shovels companies supporting quantum systems, with Q-CTRL (which raised $113M total through its October 2024 Series B-2 expansion) as the canonical portfolio reference. They note Rigetti as an exception where they invested in a quantum computer builder directly (DCVC).

Why founders pick them: DCVC's framing is clearest for enabling-infrastructure plays. If you are building control software, error correction, verification, or middleware that other quantum companies depend on, DCVC's picks-and-shovels lens is the right home.

What they scrutinize: Buyer clarity (who pays first and what budget exists), defensibility (data moat, workflow lock-in, switching costs), and adoption realism (deployment model, time-to-value, integration requirements).

How to pitch DCVC: Bring a picks-and-shovels narrative — who you sell to, what the budget owner looks like, and how you become a standard part of quantum stacks. Frame yourself as horizontal infrastructure, not a vertical application.

3. Playground Global — Capital-Heavy Hardware Conviction

Website: playground.vc

Headquarters: Palo Alto

Latest fund activity: Playground manages roughly $1.2 billion in AUM with Fund III at $410 million closed December 2023 in active deployment. Playground continued backing PsiQuantum through the company's $1 billion Series E in September 2025 at a $7 billion post-money valuation (PsiQuantum).

Stage and motion: Series A through E with check sizes scaling to $50M+ in lead positions. Playground is one of the most respected deep-tech firms for ambitious capital-heavy bets.

Key categories: Capital-intensive quantum hardware (PsiQuantum's photonic million-qubit platform is the canonical example), plus broader frontier deep-tech across robotics, materials, and infrastructure.

Why founders pick them: Conviction at scale. Playground writes large checks into multi-year hardware roadmaps and stays through follow-on rounds. The September 2025 Series E participation alongside BlackRock, Temasek, and Baillie Gifford signals continuing institutional belief in PsiQuantum's industrialization story.

What they scrutinize: Industrialization credibility (supply chain, fab partners, manufacturing timeline), team depth at the engineering and science leadership levels, and category-defining ambition (not incremental).

How to pitch Playground: Tell a credible story about industrialization. Supply chain, fab partners, timelines, and what useful means for your modality, plus how you will prove it. Bring a working physics demo plus a manufacturing-scale plan.

4. Lux Capital — Frontier VC With Real Quantum Exposure

Website: luxcapital.com

Headquarters: New York and San Francisco

Latest fund activity: Lux Capital Fund IX closed at $1.5 billion in January 2026, the firm's largest fund ever and a step up from Fund VIII at $1.15 billion (2023). Lux continues to back Rigetti Computing, listed publicly as a portfolio company building a cloud quantum computing platform (Lux).

Stage and motion: Multi-stage with check sizes from $5M-$25M depending on round. Lux backs hard-science companies and has long history with frontier hardware.

Key categories: Quantum hardware, control stacks, enabling physics tech. Lux responds best when quantum is part of a broader computing-and-physical-world narrative rather than isolated.

Why founders pick them: Pattern recognition across two decades of frontier investing, plus exceptional brand on the LP side of any later round you raise. Lux can credibly carry a hardware-heavy quantum company from Series A through growth.

What they scrutinize: Market concreteness (deep science to product to a huge real customer budget), team caliber (quantum fundraising is heavily team-driven), and contrarian conviction (Lux explicitly looks for bets that incumbents and consensus are missing).

How to pitch Lux: Make the market concrete. Lux responds well when you can connect deep science to product to a large real customer budget. Bring contrarian conviction backed by data, not just vision.

5. Amadeus Capital Partners — UK/EU Quantum + AI

Website: amadeuscapital.com

Headquarters: Cambridge and London

Latest fund activity: Amadeus runs the Amadeus V Tech Fund (£110 million) and a complementary €80M APEX climate-tech partnership. The firm continued Nu Quantum participation through the company's $60 million Series A in December 2025 (National Grid Partners led, Amadeus and IQ Capital both participated) (Amadeus).

Stage and motion: Seed through Series B with check sizes from $2M-$15M. Amadeus is one of Europe's best-known early-stage tech investors with explicit quantum language in its thesis.

Key categories: Quantum networking, distributed quantum architectures, advanced computing, and AI infrastructure. Amadeus likes founders who can show measurable progress pre-revenue (benchmarks, fidelity, integration wins).

Why founders pick them: UK/EU credibility plus a deep network across Cambridge and London quantum talent. For founders who can frame quantum as part of a broader advanced-computing shift, Amadeus is a natural fit.

What they scrutinize: Scalability (how does your approach unlock modular growth?), commercial pull (security buyers and enterprise customers are skeptical by default), and team execution (UK academic founders often need explicit go-to-market plans).

How to pitch Amadeus: Highlight scalability — how your approach unlocks modular growth like classical networking did for data centers. Show measurable pre-revenue progress and a credible commercialization plan from UK academia to US enterprise GTM.

6. IQ Capital — Cambridge Deep-Tech VC

Website: iqcapital.vc

Headquarters: Cambridge, UK

Latest fund activity: IQ Capital manages roughly $1 billion in AUM across Fund IV ($200M, June 2023) and Growth Fund II ($200M) in active deployment. The firm participates in Nu Quantum's $60M Series A and runs a deep portfolio of UK deep-tech spinouts.

Stage and motion: Seed through Series A with check sizes from $2M-$10M. IQ Capital is one of the UK's best-known deep-tech VCs and shows up in real quantum financings.

Key categories: UK and EU quantum startups, especially where Cambridge and Oxford talent pipelines matter, plus enabling tech (networking, error correction, systems software).

Why founders pick them: UK academic ecosystem credibility plus a partner bench that has scaled multiple deep-tech companies through Series B and beyond. IQ Capital's anchor in Cambridge means natural integration with the city's quantum talent flywheel.

What they scrutinize: Timeline compression (anchor on shortening the timeline to commercially relevant quantum), defensibility (what makes incumbents unable to copy you), and execution velocity (UK academic founders need to show they can ship like a company).

How to pitch IQ Capital: Anchor on shortening the timeline to commercially relevant quantum — show exactly how your product compresses that timeline. Bring concrete benchmark data, customer pilots, and a hiring plan that signals operational maturity.

7. Ten Eleven Ventures — Cyber + Quantum Crossover

Website: 1011vc.com

Headquarters: San Francisco

Latest fund activity: Ten Eleven manages over $1 billion in AUM with Fund III at $600 million (2022) in active deployment. The firm led IQM Quantum Computers' $320 million Series B in September 2025 — the largest European quantum Series B on record — alongside Tesi and additional investors (Ten Eleven).

Stage and motion: Multi-stage from seed through Series C with check sizes from $5M-$50M+. Ten Eleven explicitly positions itself as cybersecurity-dedicated but has executed a strong quantum crossover thesis through MGP Alex Doll.

Key categories: Cybersecurity native plus emerging quantum-security crossover. Ten Eleven's quantum thesis emphasizes platforms that bridge classical security workflows with post-quantum cryptography migration and quantum-resilient infrastructure.

Why founders pick them: Two decades of cybersecurity-only investing creates pattern recognition that generalists do not have, and the IQM lead signals a willingness to write very large quantum checks. For quantum founders whose buyers include CISOs and security architects, Ten Eleven's network is uniquely valuable.

What they scrutinize: ICP clarity (who buys, what budget, what trigger), cyber-buyer credibility (do CISOs see your quantum offering as security-relevant?), and platform consolidation potential (is this a feature or a category?).

How to pitch Ten Eleven: Treat your pitch like a buyer-led business case. Lead with the security-relevance pain point, the budget that exists for it, and your adoption plan. Then show your quantum wedge and what makes you defensible over a 5-year horizon.

8. In-Q-Tel — National Security Strategic Investor

Website: iqt.org

Headquarters: Arlington, Virginia

Latest fund activity: In-Q-Tel runs an explicit Microelectronics and Quantum portfolio category with active deployment across the quantum stack. Quantum portfolio includes D-Wave, Q-CTRL, Quantum Brilliance, Infleqtion, and SandboxAQ (In-Q-Tel).

Stage and motion: Strategic investor tied to the US national security ecosystem. Check sizes typically $1M-$10M+ alongside government contracting relationships.

Key categories: Quantum sensing, communications, security-relevant hardware, enabling microelectronics, and post-quantum cryptography. In-Q-Tel's portfolio reflects clear national security adoption pathways.

Why founders pick them: Defense and national security accelerator. For some quantum sub-sectors — sensing, secure communications, navigation — the public-sector adoption pathway is a credible early commercialization route, and In-Q-Tel's strategic position can compress the typical 18-24 month government sales cycle.

What they scrutinize: Mission outcomes (concrete national security applications), supply chain sovereignty (US-based components and fabrication), and operational reliability (defense-grade reliability standards, not consumer-grade).

How to pitch In-Q-Tel: Be specific about mission outcomes and deployment constraints — supply chain, sovereignty, reliability. Do not hand-wave on the defense applicability story; bring named program offices and acquisition pathways.

9. Parkwalk Advisors — UK University Spinout Powerhouse

Website: parkwalkadvisors.com

Headquarters: London

Latest fund activity: Parkwalk has deployed £496.3 million across UK university spinouts with the 5th Knowledge Intensive Fund closing in 2025/26. Quantum portfolio includes five companies: Riverlane, Nu Quantum, Phasecraft, Quantum Motion, and Oxford Quantum Circuits (Parkwalk).

Stage and motion: Seed and seed-extension with check sizes from $1M-$5M. Parkwalk is a powerhouse in UK university spinouts, which is a primary source of quantum talent and IP.

Key categories: Cambridge, Oxford, and UK-linked quantum startups across error correction (Riverlane), networking (Nu Quantum), software (Phasecraft), hardware (Quantum Motion, OQC), and broader deep-tech commercialization.

Why founders pick them: UK university spinout pipeline expertise. Parkwalk understands the university tech-transfer process, IP assignment cycles, and academic-to-commercial transition challenges that derail many spinouts. Their portfolio's quantum density signals clear domain conviction.

What they scrutinize: IP assignment clarity (clean tech-transfer is a precondition), team commercial maturity (academic founders need to ship like a company), and early commercial signal (pilots, design partners, lighthouse prospects).

How to pitch Parkwalk: Make your academic roots an advantage but show you can ship like a company — hiring plan, productization roadmap, and customer pipeline. Bring clean IP documentation showing university tech-transfer is complete.

10. Oxford Science Enterprises — Oxford Spinout Investor

Website: oxfordscienceenterprises.com

Headquarters: Oxford

Latest fund activity: OSE manages £850M+ AUM with £600M+ deployed across 80+ Oxford spinouts, with continued capital recycling from realized exits. The firm's Oxford Ionics portfolio company was acquired by IonQ for $1.075 billion in June 2025, the largest quantum-only M&A on record (IonQ).

Stage and motion: Seed through Series A with check sizes from $2M-$15M. OSE is one of the most visible university-linked investors globally, and Oxford is a quantum hotspot.

Key categories: Oxford-linked quantum startups including Oxford Quantum Circuits (superconducting hardware) plus Oxford-Ionics-style trapped-ion systems before the IonQ acquisition.

Why founders pick them: University tech-transfer expertise plus a track record of producing exit liquidity (the Oxford Ionics acquisition validates the model). For Oxford-linked spinouts, OSE is the natural first call and brings credibility with downstream Series B investors.

What they scrutinize: Spinout de-risking (clear IP assignment, product roadmap, partnerships beyond papers), team commercial capacity, and category positioning relative to Oxford's quantum research strengths.

How to pitch OSE: Show that the spinout is de-risked — clear IP assignment, a product roadmap, and partnerships that prove credibility beyond papers. Bring evidence of customer or buyer interest from outside Oxford's academic network.

11. Bpifrance — French Sovereign Quantum Capital

Website: bpifrance.com

Headquarters: Paris

Latest fund activity: Bpifrance runs the Plan Quantique €1.8 billion national programme (2021-2030) and co-led Alice & Bob's €100 million Series B in January 2025 through the Future French Champions partnership and the DeepTech 2030 fund (Alice & Bob). Bpifrance backs all five PROQCIMA programme companies (Alice & Bob, Pasqal, Quandela, C12, Quobly).

Stage and motion: Strategic investor and LP commitments from €5M-€50M+. For Europe-based quantum, Bpifrance is often the difference between great research and global-scale company.

Key categories: French and EU quantum hardware and core systems plays where serious capital and national-scale support matter. Bpifrance's thesis emphasizes sovereign quantum capability and industrialization.

Why founders pick them: Sovereign capital scale, national policy alignment, and the ability to coordinate with public procurement and EU Quantum Flagship funding. For French-headquartered quantum companies, Bpifrance is essentially mandatory at growth stage.

What they scrutinize: Industrial outcomes (manufacturing, jobs, sovereignty), credible path to a European quantum champion, and policy alignment with France's Plan Quantique objectives.

How to pitch Bpifrance: Tie your roadmap to industrial outcomes — manufacturing footprint, jobs created, sovereign capability, and a credible path to a European champion at scale. Bring policy fluency on PROQCIMA and EU Quantum Flagship alignment.

12. Novo Holdings Quantum — First Direct Quantum Software Investor

Website: novoholdings.dk

Headquarters: Copenhagen

Latest fund activity: Novo Holdings co-led Phasecraft's $34 million Series B in September 2025 alongside Plural and Playground Global — described publicly as Novo's "first direct quantum software investment" (Phasecraft). The Novo Holdings Quantum fund signals institutional Nordic capital entering the sector.

Stage and motion: Series A through B with check sizes from $5M-$25M. Novo brings Nordic LP credibility and a long-duration capital base aligned with quantum's multi-year roadmap.

Key categories: Quantum software, algorithms, and applied chemistry/biology where Novo's life-sciences DNA creates pattern recognition. The Phasecraft investment focuses on application-layer quantum software for materials and chemistry.

Why founders pick them: Nordic institutional credibility, long-duration capital, and deep life-sciences and chemistry domain expertise. For quantum applications in pharma, materials, and chemistry, Novo's network is uniquely valuable.

What they scrutinize: Application-layer credibility (real chemistry, materials, or pharma use cases), team depth in both quantum and the application domain, and commercial pull from enterprise customers.

How to pitch Novo: Lead with application credibility — concrete chemistry, materials, or biology problems your quantum approach unlocks. Bring enterprise pilots and named scientific advisors who connect quantum capability to real-world R&D budgets.

The Eight Days That Reshaped Quantum Capital (September 2-10, 2025)

September 2-10, 2025 is the most consequential eight-day window in private quantum financing history. Four rounds totaling roughly $1.95 billion closed across the window, with one round in each major modality (software, superconducting, trapped-ion, photonic). This was the moment institutional capital declared its conviction in quantum platforms.

| Date | Company | Round | Amount | Modality | Lead investor |

|---|---|---|---|---|---|

| September 2 | Phasecraft | Series B | $34M | Quantum software | Plural + Playground + Novo |

| September 3 | IQM | Series B | $320M | Superconducting hardware | Ten Eleven Ventures |

| September 4 | Quantinuum | Strategic | $600M | Trapped-ion hardware | Quanta + NVentures + JPM |

| September 10 | PsiQuantum | Series E | $1,000M | Photonic hardware | BlackRock + Temasek + Baillie Gifford |

What the eight-day window tells founders pitching in 2026: Institutional capital is now writing $300M+ checks into quantum hardware platforms with credible industrialization roadmaps. Quanta Computer's lead in Quantinuum at a $10 billion pre-money valuation, BlackRock and Temasek participating in PsiQuantum at $7 billion post-money, and Ten Eleven leading IQM at $320M all signal that quantum has crossed the threshold from venture-only to mixed venture-and-institutional capital. The bar to compete for this tier is high — a credible physics roadmap, working hardware demos, named enterprise pilots, and a clear path to industrialization — but the capital is genuinely available for platforms that clear it.

The Q1 2026 pullback to roughly $240 million in global quantum VC (per New Market Pitch) is best read as a barbell signal: post-September 2025 mega-rounds, capital concentrates at the top while the long tail tightens. For founders raising in 2026, this means specialist VCs with fresh dry powder (Quantonation Fund II, Lux Fund IX, DCVC's 2024 closes) and crossover capital (Ten Eleven, Novo Holdings) are the most active sources.

Quantum Capital Intensity Tiers (2026 Framework)

Quantum funding is segmented by capital intensity. The four-tier framework below maps typical round sizes to investor profiles, helping founders quickly identify which firms write checks in their tier.

| Tier | Typical round | Modality | Active investors | 2025-2026 example rounds |

|---|---|---|---|---|

| Tier 1 — Hardware platforms | $500M-$2B+ | Photonic, superconducting, trapped-ion at scale | Playground, BlackRock, Temasek, Quanta, Bpifrance | PsiQuantum $1B Sept 2025; Quantinuum $600M Sept 2025 |

| Tier 2 — Hybrid hardware | $60M-$300M | Hardware companies with revenue or acquisition pathway | Ten Eleven, Lux, In-Q-Tel, OSE, Bpifrance, FFC partnership | IQM $320M Sept 2025; Multiverse $215M June 2025; QuEra $230M Feb 2025; Infleqtion $100M June 2025 |

| Tier 3 — Software + tooling | $10M-$100M | QEC, control, networking, simulation, optimization | DCVC, Quantonation, Amadeus, IQ Capital, Novo, Parkwalk | Phasecraft $34M Sept 2025; Nu Quantum $60M Dec 2025; Q-CTRL $113M total Oct 2024 |

| Tier 4 — Sensing + niche | $5M-$50M | Timing, gravimetry, imaging, post-quantum crypto | In-Q-Tel, Quantonation, Amadeus, Parkwalk | Niche sensing and PQC plays funded across In-Q-Tel + EU sovereign quantum programmes |

Hands-on observation from quantum fundraises that have moved through Peony in 2025-2026: the median diligence data room contains 280+ documents — IP filings and patent docket, supplier and fab dependencies, experimental data with fidelity benchmarks, milestone roadmaps, security posture and export-control compliance, and standard financials. Peony's page-level analytics let quantum founders see which VCs actually read the experimental data section versus just the executive summary. And per Peony's 2026 VDR pricing research, 47% of Western VDRs hide pricing entirely — a real tax on quantum founders who need predictable cost structures while running concurrent fundraising and enterprise sales processes.

How do I actually pitch a quantum VC in 2026? (5 tactical tips)

Lead with a concrete physics milestone ladder and a buyer-pull story, not vision-statement category claims. Quantum specialists have seen hundreds of physics-roadmap pitches — the five tips below separate a funded round from a polite pass.

1. Show your physics milestone ladder

Investors want to see 3-5 technical milestones that de-risk the next round — error rates, fidelity, scaling approach, integration depth, stability under operating conditions. Make every milestone measurable and tie it to a specific calendar quarter. A milestone ladder that shows "we will achieve 99.9% gate fidelity by Q3 2026 and demonstrate logical qubit error correction at scale by Q1 2027" is materially more credible than "improve fidelity over time."

2. Translate quantum performance into buyer value

Even pre-revenue, you should know who pays first, why they pay, and what success looks like. Speedup, accuracy, cost reduction, security posture — pick the dimension that maps to your buyer's budget. Quantum advantage is a research-paper concept; quantum buyer value is what gets you funded.

3. Be explicit about what you are not doing

Quantum investors respect focus. If you are not building full-stack hardware, say so. If you are, show why that is necessary and defensible. Sponsor preferences vary sharply — DCVC's picks-and-shovels framing rewards clarity on horizontal infrastructure; Playground and Lux reward conviction on vertical hardware platforms.

4. Make your go-to-market before quantum advantage real

Many winning quantum companies sell enabling layers (tooling, control, networking, error correction) before full fault tolerance arrives. DCVC's picks-and-shovels lens is a strong mental model to address directly. For software and applications companies, the bridge revenue from classical hybrid use cases (Multiverse's $215M Series B in June 2025 demonstrates this pattern) is increasingly important to investor diligence.

5. Bring the diligence pack like a grown-up lab founder

Have ready: IP status with patents and licensing, key hires, supplier dependencies and fab partners, experimental data with fidelity benchmarks, security posture documentation, export-control compliance, and a realistic budget tied to milestones. Use a professional data room like Peony to organize materials with AI-powered organization and track investor engagement with page-level analytics — Google Drive cannot index complex deep-tech diligence packs and DocSend has no NDA workflow at all.

Why does a data room matter more for quantum founders than other startups?

Because you are pitching investors on a multi-decade physics roadmap while sharing your most sensitive IP — patent filings, experimental data, fab partnerships, export-controlled technical specifications — and the delivery mechanism is part of your credibility story. There is a specific irony in quantum fundraising: founders who pitch breakthrough physics through unprotected Google Drive links. Investors notice, and export-control regulators notice harder.

Peony was built for exactly this tension. A quantum founder sharing IP through a Peony data room gets:

- Screenshot protection that blocks and logs capture attempts — so leaked screenshots trace back to the source viewer, critical for export-control compliance

- Dynamic watermarks tied to each viewer's identity, embedded in every page view — every investor sees a personalized watermark

- Page-level analytics showing exactly which documents each investor reviewed, how long they spent per page, and how many times they returned

- NDA gates that require identity verification before access — investors self-serve, you do not grant permissions manually at midnight

- AI auto-indexing that organizes uploaded documents into deal-ready folder structures in under 3 minutes, including IP/patents, experimental data, milestone roadmap, and team credentials sections

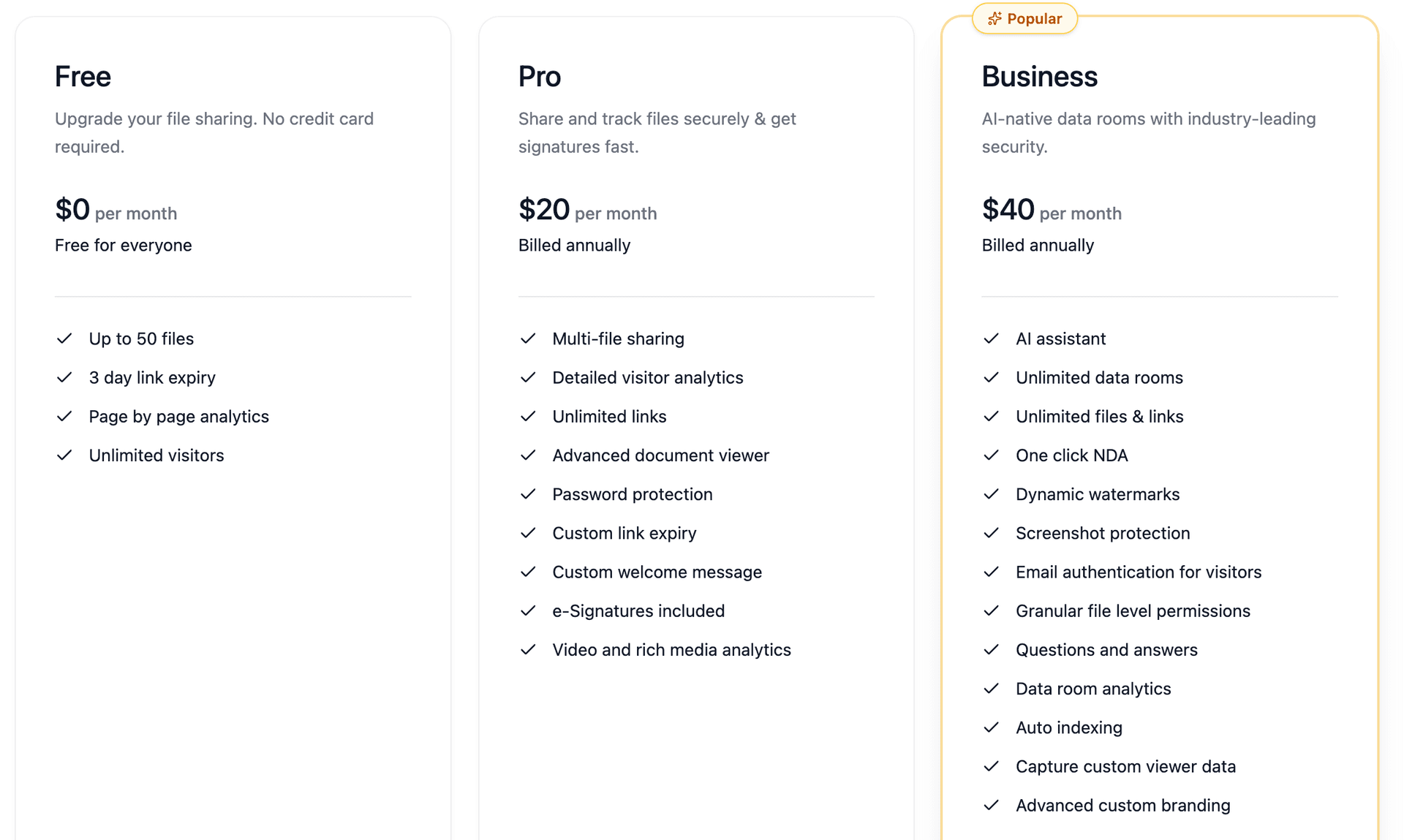

You set it up in under five minutes, not weeks. Pricing is transparent: Business at $40/admin/month includes all security and AI features, Pro at $20/admin/month covers core analytics and e-signatures — versus $5,000-$20,000 per-deal costs of legacy platforms like Datasite or Intralinks. For a 3-person quantum founding team running a seed round, that is $60-$120/month versus thousands.

For quantum founders specifically, how you handle sensitive materials is part of your credibility story. A secure data room is not just a convenience — it is a signal of operational discipline that quantum investors actively value when they evaluate you.

How much capital actually flowed into quantum startups in 2025-2026?

| Metric | Value | Source |

|---|---|---|

| Total private quantum VC in 2025 | $4.9 billion (+192% YoY from $1.7B in 2024) | QED-C 2026 |

| Q1 2025 quantum VC | $1.25B+ (+128% YoY) | Crunchbase News |

| Q1 2026 global quantum VC | ~$240 million (post-September 2025 pullback) | New Market Pitch |

| Pure-play quantum companies | 556 tracked (7,418 quantum-engaged) | QED-C 2026 |

| Cumulative public-sector quantum | $56.7 billion (+$12.7B in 2025) | QED-C 2026 |

| US National Quantum Initiative | $2.7B over FY2025-FY2029 (NQI Reauthorization 2026) | Senate S.3597 |

| UK National Quantum Strategy | £2.5B over 10 years + £1B ProQure procurement | UK gov publication |

| France Plan Quantique | €1.8B (2021-2030) + PROQCIMA programme | Bpifrance |

| EU Quantum Europe Strategy | Adopted July 2, 2025 | European Commission |

| Largest quantum-only M&A 2025 | IonQ acquires Oxford Ionics for $1.075B (June) | IonQ |

| Largest 2025 quantum private round | PsiQuantum $1B Series E at $7B post-money (Sept 10) | PsiQuantum |

| Largest European quantum round | IQM $320M Series B Sept 3 2025 (Ten Eleven lead) | Ten Eleven |

| September 2025 mega-round window | $1.95B in 8 days across 4 rounds | Aggregated from primary announcements |

| Quantinuum IPO readiness | Confidential IPO registration signaled in 2026 | Quantinuum |

The takeaway: more capital is going into fewer companies with stronger industrialization roadmaps. If you are in the running, the opportunity is enormous. If you are not, the bar to get in is higher than it has ever been — and the data room you bring to that first meeting is part of how you signal you belong.

Frequently Asked Questions

I am a quantum hardware founder raising a $10M Series A — which investors actually lead rounds in quantum computing?

Quantonation is the most recognized quantum-dedicated VC globally and closed Quantonation II at €220 million in February 2026 (final close, oversubscribed) — the specialist benchmark for quantum rounds. DCVC closed over $700M across DCVC Climate and DCVC Bio III in late 2024 and runs an explicit picks-and-shovels quantum thesis with Q-CTRL and Rigetti in portfolio. Playground Global backs PsiQuantum's $1B Series E (closed September 2025, $7B post-money valuation) for utility-scale fault-tolerant quantum computing. Lux Capital's Fund IX closed at $1.5 billion in January 2026 — the firm's largest ever — with continued frontier hardware exposure including Rigetti. Ten Eleven Ventures led IQM Quantum Computers' $320M Series B in September 2025, the largest European quantum Series B on record. For European hardware, Bpifrance co-led Alice & Bob's €100M Series B in January 2025 through France's PROQCIMA programme. Peony data rooms let you share your physics milestone ladder, IP docket, and financial model with all these investors simultaneously through NDA-gated links while page-level analytics show which partners actually read your fidelity benchmarks versus skimming the executive summary.

I am raising seed funding for a quantum software startup — what check sizes do quantum investors typically write?

Quantum investor check sizes vary dramatically by category and stage. Quantonation focuses on seed-stage from the €220M Fund II (final close February 2026) writing $1M-$5M initial cheques. DCVC and Lux Capital write $5M-$25M+ multi-stage cheques on the picks-and-shovels enabling layer. Amadeus Capital Partners (Amadeus V Tech Fund £110M) and IQ Capital (Fund IV $200M, June 2023) write $2M-$10M at seed-Series A in UK and EU quantum. Playground Global makes the largest bets — Fund III $410M, $1.2B AUM — at later hardware-heavy stages like the PsiQuantum $1B Series E. Parkwalk Advisors specializes in UK university spinouts (Riverlane, Nu Quantum, Phasecraft, Quantum Motion, OQC) at $1M-$5M tickets. Oxford Science Enterprises backs Oxford-linked startups including Oxford Ionics (acquired by IonQ for $1.075 billion in June 2025). For quantum software and tooling companies the capital intensity is lower so seed rounds of $2M-$5M are common with DCVC's picks-and-shovels framing being a strong match. With Peony at $40 per admin per month your entire data room costs less than a single conference dinner — Google Drive folders give you zero tracking on who opened what, and DocSend has no NDA workflow at all.

I am a quantum sensing founder spinning out of a Cambridge lab — how should I approach quantum investors?

For Cambridge spinouts Parkwalk Advisors is the natural first call — they manage £496.3 million deployed across UK university spinouts and run five quantum portfolio companies including Riverlane, Nu Quantum, Phasecraft, Quantum Motion, and OQC. IQ Capital is another Cambridge-anchored deep-tech VC active in quantum with Fund IV at $200M plus Growth Fund II at $200M (combined $1B AUM) and participates in Nu Quantum alongside Amadeus. Amadeus Capital Partners invests in quantum and advanced computing pioneers from the Amadeus V Tech Fund (£110M) plus the €80M APEX climate-tech partnership. Your approach should lead with the physics wedge plus the commercial wedge simultaneously because quantum investors pattern-match hard. For sensing specifically, show that your approach is nearer-term revenue — timing, gravimetry, and imaging often have faster paths to buyers than computing. Make your academic roots an advantage but show you can ship like a company with a hiring plan, productization roadmap, and customer pipeline. Peony AI-powered document organization auto-indexes your IP filings, experimental data, patent docket, and milestone plans into a professional data room in under 3 minutes — versus emailing loose PDFs through Dropbox where you cannot tell if anyone actually reviewed your patent claims.

I am pitching DCVC and Quantonation for our quantum middleware company — what do quantum investors expect in a data room?

Quantum investors expect a data room that mirrors a grown-up lab founder's diligence pack including IP status with patents and licensing, key hires and team credentials, supplier dependencies and fab partners, experimental data with benchmarks and fidelity metrics, a realistic budget tied to technical milestones, security posture documentation including export-control posture, and standard financials. DCVC specifically wants to see a picks-and-shovels narrative showing who you sell to, what the budget owner looks like, and how you become a standard part of quantum stacks (Q-CTRL is the canonical portfolio reference). Quantonation wants the physics wedge plus the commercial wedge explaining why your roadmap makes the useful quantum timeline shorter for specific problems. Include 3 to 5 technical milestones that de-risk the next round covering error rates, fidelity, scaling approach, integration, and stability. Sharing this through Google Drive or DocSend means you have no idea which pages each partner reviewed or how long they spent on your experimental data. Peony page-level analytics show exactly which documents each investor reviews and for how long, and dynamic watermarks trace any document leak back to the specific viewer — at $40/admin/month for Business tier versus $5,000+ per deal for legacy platforms like Datasite.

I am a quantum startup sharing sensitive IP and experimental data with six investors — how do I securely share my pitch materials?

Quantum IP is among the most sensitive startup documentation given patent races, US and EU export controls, and national security implications. Never email unprotected experimental data and patent applications to multiple investors simultaneously. Set up a single data room with separate NDA-gated access links for each investor so you control who sees what and when. Peony provides enterprise-grade security including identity-bound access that ties every document view to a verified viewer, dynamic watermarks that embed the viewer's name into every rendered page, screenshot protection that blocks and logs unauthorized capture attempts, and link expiry with instant access revocation if a conversation goes cold. This matters especially when sharing with strategic investors like In-Q-Tel (which runs an explicit Microelectronics and Quantum portfolio category covering D-Wave, Q-CTRL, Quantum Brilliance, Infleqtion, and SandboxAQ) where defense and national security sensitivity is heightened. At $40 per admin per month for Business tier this costs a fraction of what legacy platforms charge per deal while giving you more granular control than Dropbox shared folders where anyone can forward the link without your knowledge.

I am raising a quantum Series A — how long does the typical quantum fundraise take from first meeting to close?

Quantum fundraises typically take longer than software rounds because technical diligence is deeper and syndicate construction is more complex. Expect 12 to 20 weeks for a Series A with specialist quantum investors, though enabling-layer companies with nearer-term revenue like tooling, control software, or error correction can move faster at 8 to 14 weeks. Hardware and systems companies with capital-heavy roadmaps often need larger syndicates which extends timelines — see Quantinuum's $600M round at $10B pre-money in September 2025 (Quanta Computer + NVentures + QED Investors + JPMorgan), where the syndicate alone took months to assemble. The fastest path is targeting investors with published quantum theses and fresh dry powder since new funds and new closes mean faster decisions and more follow-ons. Quantonation Fund II's €220M February 2026 final close, DCVC's $700M+ late-2024 close across Climate + Bio III, Lux Capital Fund IX's $1.5B January 2026 close, and Ten Eleven's active third fund all signal active deployment. Prepare your 3 to 5 physics milestone ladder upfront so technical diligence does not stall the process. Peony page-level analytics let you monitor real-time engagement so you know which investors are actively reviewing documents and can time your follow-ups to maximize momentum rather than guessing who among six simultaneous conversations is actually interested.

I am building a quantum error correction startup — which investors focus on specific quantum sub-sectors?

Quantum investors pattern-match by sub-sector so targeting matters enormously. For error correction and runtime, Parkwalk Advisors backs Riverlane (which raised $75M+ in August 2024 to build the operating system for error-corrected quantum computers) and Phasecraft (which closed $34M Series B in September 2025 with Plural and Playground co-leading alongside Novo Holdings' first direct quantum software investment). For quantum networking and distributed architectures, Amadeus Capital Partners and IQ Capital both invested in Nu Quantum's $60M Series A in December 2025 (National Grid Partners led). For picks-and-shovels enabling infrastructure, DCVC is the clearest match with Q-CTRL ($113M total funding through October 2024 Series B-2 expansion). For capital-intensive hardware, Playground Global backs PsiQuantum's $1B Series E and Lux Capital has Rigetti Computing. For superconducting and trapped-ion at scale, Ten Eleven Ventures led IQM's $320M Series B in September 2025. For defense and national security applications, In-Q-Tel runs an explicit Microelectronics and Quantum portfolio category. For European quantum champions, Bpifrance participates through its Plan Quantique €1.8B programme and the PROQCIMA initiative seeded five French hardware champions (Alice & Bob, Pasqal, Quandela, C12, Quobly). Peony AI-powered document organization handles the sub-sector-specific documentation quantum startups need — error rate benchmarks, fidelity data, and integration specifications alongside standard financials — which Google Drive cannot organize or track.

I am comparing data room options for my quantum fundraise — what is the best data room for quantum startup fundraising?

For quantum startup fundraising you need a data room that handles sensitive IP and experimental data securely, sets up fast so you focus on the physics rather than document management, and provides analytics to track investor engagement across a complex syndicate. Peony sets up a complete investor data room in under 5 minutes with AI-powered document organization that auto-indexes your technical architecture, IP and patents, experimental data, financial projections, and milestone plans into a professional folder structure. Page-level analytics show which documents each investor reviews and for how long, dynamic watermarks embed viewer identity into every page, screenshot protection blocks unauthorized capture of sensitive IP, and NDA gates control access before anyone sees materials. At $40 per admin per month for Business tier a 3-person founding team pays $120 per month total versus $5,000 to $20,000 per deal for legacy platforms like Datasite or Intralinks. DocSend gives you basic link tracking but no watermarking, no screenshot protection, and no AI organization. Google Drive and Dropbox offer no analytics at all. For a quantum startup where IP security is existential and export controls are real, Peony delivers enterprise features at startup pricing — and unlike Datasite, Peony sets up in under 5 minutes with no sales call.

Our quantum startup raised in 2024 and now we are raising a Series B in 2026 — has the market actually changed for quantum founders?

Yes, materially. Private VC into quantum hit $4.9 billion in 2025, up 192 percent year-over-year per QED-C's State of the Global Quantum Industry 2026 — and 2025 saw three back-to-back mega-rounds in September alone (IQM $320M on September 3, Quantinuum $600M on September 4, PsiQuantum $1B on September 10) totaling $1.92B in just eight days. By contrast, Q1 2026 global quantum VC came in at roughly $240M per New Market Pitch — a sharp pullback from the September 2025 mega-round window, suggesting a barbell market where elite hardware platforms attract concentration capital while the long tail tightens. Public-sector commitments cumulatively reached $56.7B by end of 2025 (up $12.7B in the year), with the US National Quantum Initiative reauthorization adding $2.7B over FY2025-FY2029, the UK National Quantum Strategy committing £2.5B over 10 years plus a £1B ProQure procurement programme, France's Plan Quantique at €1.8B, and the EU's Quantum Europe Strategy adopted in July 2025. For your Series B specifically, this means investors will benchmark you against the September 2025 reference rounds — and your data room needs to clear that diligence bar. Peony at $40/admin/month gives you the enterprise security and AI auto-indexing that legacy platforms charge $20K+ per deal for.

I am evaluating whether quantum is too capital-intensive for my LP base — what does the 2025 acquisition data tell me?

The 2025 quantum M&A data tells a clear story: capital is flowing into category consolidation, and select hardware companies have liquidity paths. The largest single 2025 quantum-only M&A was IonQ acquiring Oxford Ionics for $1.075 billion in June 2025, validating Oxford Science Enterprises' spinout-investing thesis. IonQ ran a broader $2.5 billion M&A blitz over 12 months including Capella Space, Vector Atomic, Lightsynq, an ID Quantique majority stake, and Qubitekk — meaning quantum acquirers are actively rolling up the stack. D-Wave executed a $400M ATM equity raise at an average $15.18 per share in June 2025, demonstrating continued public-market quantum demand. Quantinuum has signaled confidential IPO readiness in 2026, signaling that the largest private quantum-computing companies are now genuinely IPO-ready. From an LP perspective the read is: quantum hardware is genuinely capital-heavy with longer hold periods (8-12 years versus 5-7 for SaaS) but liquidity exists for category leaders, and the 192 percent YoY private VC growth signals returning institutional risk appetite. For sub-sector exposure with shorter cycles, software and tooling companies (DCVC's picks-and-shovels thesis, Quantonation seed plays) offer faster Series A-to-exit paths. Peony at $40/admin/month is how dual-strategy quantum funds run parallel deal rooms across hardware and software portfolio companies without paying enterprise VDR fees.

Related Resources

You might also like

Apr 1, 2026

Top 15 Deep Tech VCs Writing $2M-$100M Checks (Sizes Inside) in 2026

Apr 29, 2026

Top 8 Boston Investors in 2026: The Founder's Complete Guide to Raising in Boston & Cambridge

Apr 29, 2026

Top 10 Active Investors in Italy (2026): Complete Founder Guide to Italian VC Firms